The marketplace for commercial insurance will continue to favor insurance buyers in 2017, particularly those with strategic risk management and risk transfer strategies, according to Willis Towers Watson’s 2017 Marketplace Realities report.

The report points to strong marketplace capacity as a key driver in market conditions and contends that this ample capacity will likely allow insurers to absorb any natural catastrophe losses in 2016, including those from Hurricane Matthew and the Atlantic hurricane season.

Overall, buyers’ individual risk profiles will determine their fate at the negotiating table, according to the report. But in general, downward or stable pricing will continue for most property and general liability risks, while certain lines such as cyber, auto liability and health insurance will see rate increases.

“The mix of increases and decreases, while subject to some change line by line, overall remains steady,” said Matt Keeping, Willis Towers Watson head of broking, North America. “The marketplace continues to offer opportunities for buyers, but as always, strategic planning yields the best results. The key point for buyers is to understand the nuances of the market so they can optimize their risk management programs.”

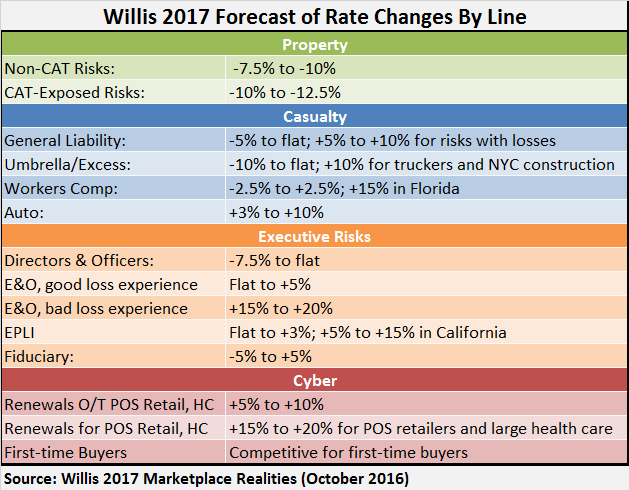

In property lines, the ongoing declining rate trend continues, according to the report. Catastrophe-exposed programs, having led the softening cycle last year, continue to lead the declines. Property rates are expected to decline 7.5 percent to 10 percent for companies without significant exposure to natural disasters and 10 percent to 12.5 percent for those more exposed.

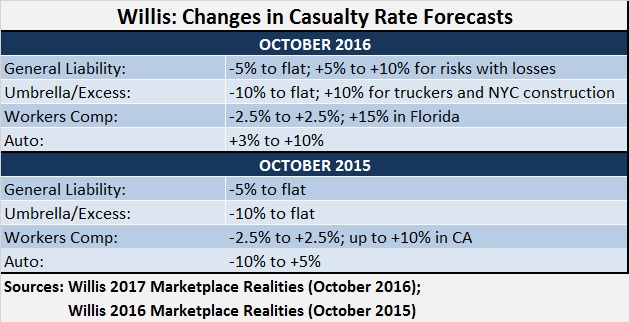

For general liability, rates for 2017 are expected to be down 5 percent to flat, although buyers with recent claims can anticipate increases of 5 percent to 10 percent.

Workers compensation costs are forecast to remain steady, with small increases or decreases for most buyers.

In the auto liability line, an increase in the frequency and severity of losses is driving up rates as much as 10 percent. International casualty rates are predicted to remain flat or fall by up to 10 percent.

Cyber renewals are facing primary premium increases of 5 percent to 10 percent for most buyers, and 15 percent to 20 percent for point-of-sale retailers and large health care companies with no loss experience. For organizations with strong risk controls, premium increases can be lessened. Organizations that operate in the middle-market space (annual revenues below $1 billion) can expect a very competitive cyber-market with aggressive pricing and broad policy language, as many carriers are eager to write these accounts, the authors of the report said.

In executive risk lines, buyers will continue to find a mix of modest increases and decreases, with rate increases driven largely by adverse risk profiles. For example, in the errors and omissions market, large technology companies with new media and service offerings can expect to see rate increases due to expanding global privacy laws. Meanwhile, the directors and officers liability market remains robust as insurers roll out coverage enhancements and buyers are obtaining unprecedented value in the trade-off between terms and price, according to the report.

“While insurance companies have been struggling to achieve the level of growth that shareholders and industry analysts hope to see, the overall stability of the industry—its ability to absorb losses, pay claims following catastrophes and support sustainable business growth—is a positive sign,” Keeping said.

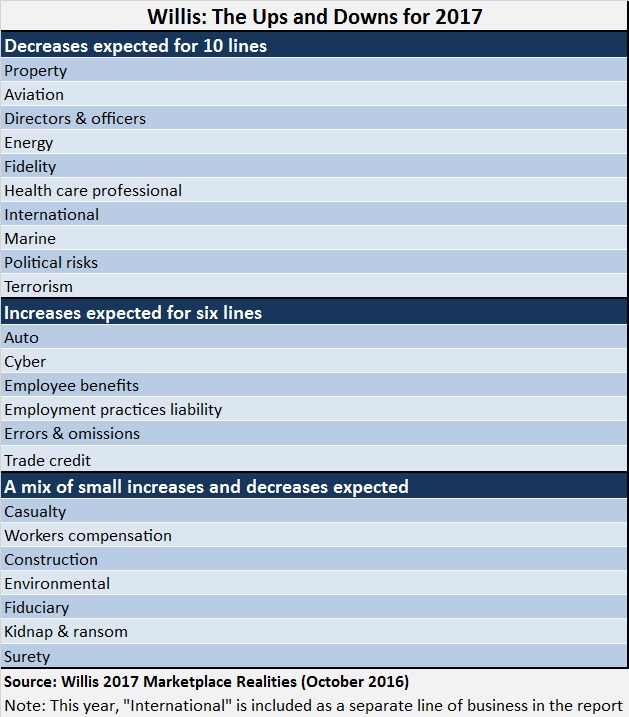

The report summarizes lines for which increases and decreases are expected each year. The most notable change from last year’s report moves the auto line into the “increases” category. Willis Towers Watson had predicted a mix of small increases and decreases for the auto line in its forecast for 2016 published in October 2015. Casualty, for which decreases were forecast in the prior report, will see smaller decreases and some increases in 2017, the report says.

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz