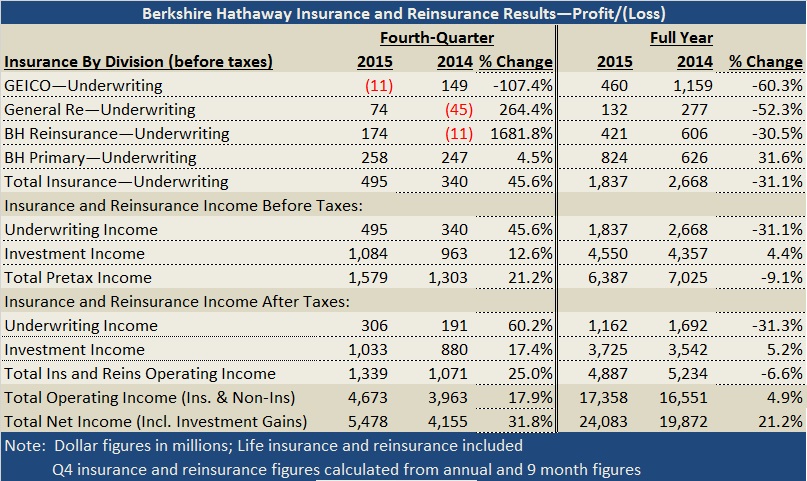

Insurance operations contributed $4.9 billion to total operating income of $17.4 billion for Berkshire Hathaway in 2015, with underwriting profit levels dropping and investment income rising compared to 2014.

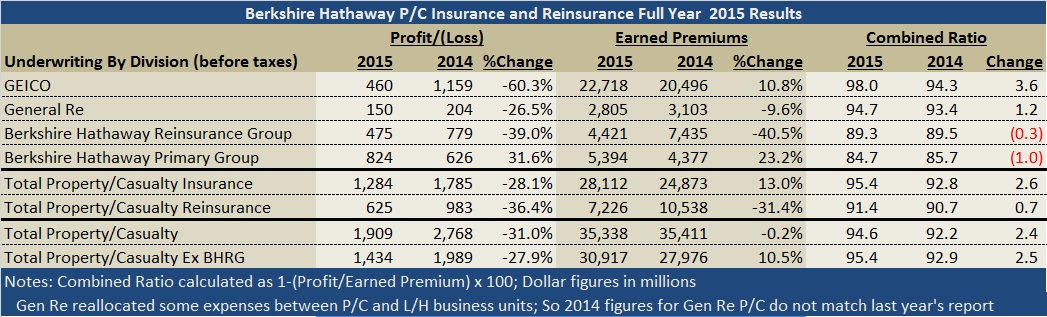

The underwriting component, $1.2 billion (after taxes), represented the 13th straight insurance underwriting profit for the Nebraska-based conglomerate. But the amount was more than 30 percent lower than in 2014 as GEICO, General Re and Berkshire Hathaway Reinsurance all reported smaller margins of underwriting profit in 2015.

Only Berkshire’s primary operation posted a higher level of underwriting profit—$824 million (before taxes), nearly 32 percent higher than 2014—while profits for GEICO and the reinsurance operations dropped between 30 percent and 60 percent. Results for just the P/C insurance operations and the P/C operations of the reinsurance operations are set forth in the chart below.

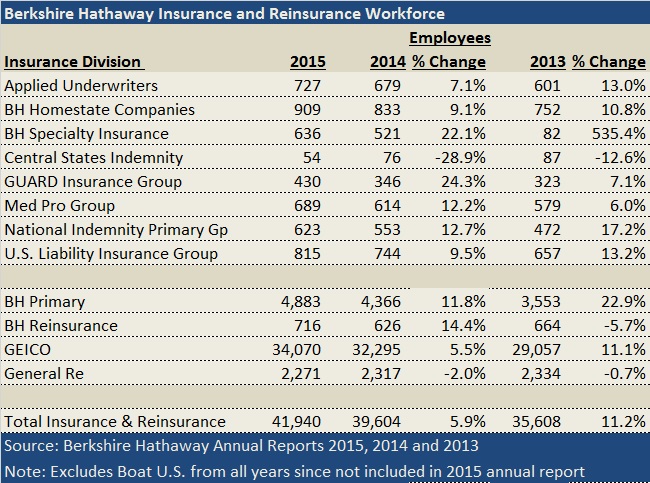

Although the annual report does not break out results for the individual commercial primary insurance operations, which include MedPro Group (providers of medical malpractice), National Indemnity Co.’s primary group (writers of commercial auto and general liability), Berkshire Hathaway Homestate Cos. (providers of commercial multiline insurance, including workers compensation), GUARD Insurance (providers of workers compensation and commercial P/C insurance to small and midsize businesses), and Berkshire Hathaway Specialty Insurance, Warren Buffett called out the contributions of BH Specialty and President Peter Eastwood, in his annual letter.

“BHSI has already developed $1 billion of annual premium volume and, under Peter’s direction, is destined to become one of the world’s leading P/C insurers,” said Buffett, chairman and CEO of the conglomerate that includes the specialty insurance operation.

Buffett first predicted the billion-dollar premium milestone in his 2013 annual letter in March 2014. “BHSI will be a major asset for Berkshire, one that will generate volume in the billions within a few years,” he wrote back then when BHSI had just 82 employees. Now the unit has a workforce of more than 600 people. (See chart of employees by unit later in this article).

In 2015, earned premiums for all the primary commercial operations, including BHSI, grew 23 percent to $5.4 billion. The primary group also posted an 84.7 combined ratio for the year—the lowest of the four divisions broken out in Berkshire’s annual report.

“In aggregate, these companies are a large, growing and valuable operation that consistently delivers an underwriting profit, usually much better than that reported by their competitors. Indeed, over the past 13 years, this group has earned $4 billion from underwriting—about 13 percent of its premium volume,” Buffett wrote.

According to Buffett’s annual letter, underwriting profit for all of Berkshire’s insurance and reinsurance totaled $26 billion during the 13-year period run of consecutive underwriting results above breakeven. “We’ve spent 48 years building this multifaceted operation, and it can’t be replicated,” he said.

The oldest of the insurance operations—GEICO—also reported double-digit premium growth (of just about 11 percent) in 2015, but the auto insurer’s combined ratio jumped almost 4 points for the year (to 98.0). Claims frequencies and severities both increased, Berkshire said in the management discussion section of the annual report, attributing the changes to increases in miles driven, repair costs, medical costs and weather conditions.

For the fourth quarter, GEICO was the only property/casualty insurance division of Berkshire to post a small underwriting loss with a combined ratio just over 100.

Reinsurance Pressured

“Today, our insurance results are likely to be more stable than was the case a decade or two ago because we have deemphasized catastrophe coverages and greatly expanded our bread-and-butter lines of business,” Buffett wrote early in his letter. “You should recognize, however, that underwriting in any given year could well be unprofitable, perhaps substantially so.”

That wasn’t the case for 2015 as the P/C operations of both General Re and Berkshire Hathaway Reinsurance recorded underwriting profits for the full year and the fourth quarter in 2015. The text of the financial report, however, noted the impact of losses from an explosion in Tianjin, China for both companies ($50 million for Gen Re and $86 million BHRG) contributed to lower profit numbers in 2015.

As in past years, Buffett’s letter praised Ajit Jain, the leader of Berkshire Hathaway Reinsurance Group, and General Re’s Tad Montross for the disciplined risk selection of the reinsurance groups. The letter also continued the tradition of contrasting Berkshire’s successful run of profitability for the insurance and reinsurance operations overall to the industry trends.

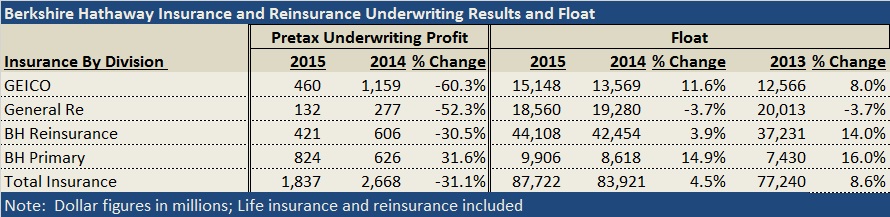

“Berkshire’s huge and growing insurance operation again operated at an underwriting profit in 2015—that makes 13 years in a row—and increased its float. During those years, our float—money that doesn’t belong to us but that we can invest for Berkshire’s benefit—grew from $41 billion to $88 billion.”

“Unfortunately, the wish of all insurers to achieve this happy result creates intense competition, so vigorous indeed that it sometimes causes the P/C industry as a whole to operate at a significant underwriting loss,” Buffett wrote, explaining that this loss is what the industry pays to hold its float. “Competitive dynamics almost guarantee that the insurance industry, despite the float income all its companies enjoy, will continue its dismal record of earning subnormal returns on tangible net worth as compared to other American businesses,” he said.

A prolonged period of low interest rates is exacerbating profit problems for insurers and “virtually guarantees that earnings on float will steadily decrease for many years to come,” Buffett said, highlighting particular pressures for reinsurers.

“It’s a good bet that industry results over the next ten years will fall short of those recorded in the past decade, particularly for those companies that specialize in reinsurance,” the letter said.

Move Over State Farm

While both reinsurance businesses reported declines in premium volume, business is growing at both GEICO and the commercial primary insurers. And employee counts for the insurance groups rose as well. GEICO has added over 5,000 employees in the past two years, and the commercial insurers have added more than 1,000. The counts by company are shown individually on the chart below.

Now more than 34,000 strong, GEICO is on a path to overtake State Farm as the largest auto insurer by premium volume in less than 15 years. “With the price advantage GEICO’s low costs allow, it’s not surprising that several years ago the company seized the number-two spot in auto insurance from Allstate. GEICO is also gaining ground on State Farm, though it is still far ahead of us in volume. On August 30, 2030—my 100th birthday—I plan to announce that GEICO has taken over the top spot. Mark your calendar,” Buffett wrote.

Recounting the story of how USAA employees Leo and Lillian Goodwin started Government Employees Insurance Co. (now GEICO) in 1936—with the dream of broadening the USAA target market for its direct distribution model beyond military officers and $100,000 of capital—Buffett reported that GEICO’s $23 billion is now more than twice USAA’s volume.

Both insurers are taking full advantage of the low-cost operating model, Buffett said, noting GEICO’s underwriting expense ratio of 14.7 in 2015. USAA’s is lower, he said, parenthetically remarking that GEICO “is fully as efficient as USAA but spends considerably more on advertising aimed at promoting growth.”

Comparing the efficiency of direct writers to the captive agency writers like State Farm, Buffett referred specifically to GEICO’s 34,000-member workforce employed to serve its 14 million policyholders. “I can only guess at the workforce it would require to serve a similar number of policyholders under the agency system. I believe, however, that the number would be at least 60,000, a combination of what the insurer would need in direct employment and the personnel required at supporting agencies.”

“At some point in the future—though not, in my view, for a long time—GEICO’s premium volume may shrink because of driverless cars. This development could hurt our auto dealerships as well,” he wrote. (Emphasis added by Buffett.)

Berkshire’s Overall Results; Fourth-Quarter Numbers

For 2015, after-tax operating earnings for all Berkshire’s businesses—insurance and noninsurance—totaled $17.4 billion.

Adding investment and derivative gains to operating earnings, total bottom-line net earnings were $24.1 billion in 2015, up 21.1 percent compared to a $19.9 billion figure in 2014.

For the fourth quarter, after-tax operating income jumped 25 percent for insurance and reinsurance businesses to $1.3 billion, with $1.0 billion of investment income making up the bulk of the figure. Investment income for the quarter grew 17.4 percent. After-tax underwriting profits also grew 60 percent to $306 million with a reversal from an underwriting loss to a profit at Berkshire Hathaway Reinsurance accounting for most of the gain.

Total operating earnings for all Berkshire’s businesses rose 17.9 percent to nearly $4.7 billion in the quarter. Net earnings, including higher investment and derivative gains for the quarter, brought the fourth-quarter 2015 bottom line up to $5.5 billion—31.8 percent higher than fourth-quarter 2014.

Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  Raised on Breaches, Digital Natives Think Differently About Cyber Risk

Raised on Breaches, Digital Natives Think Differently About Cyber Risk  Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal

Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal  California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles

California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles