In a year-end report on the U.S. excess and surplus lines market, data compiled by Fitch Ratings revealed that the top growing E&S writers in recent years were not necessarily the biggest.

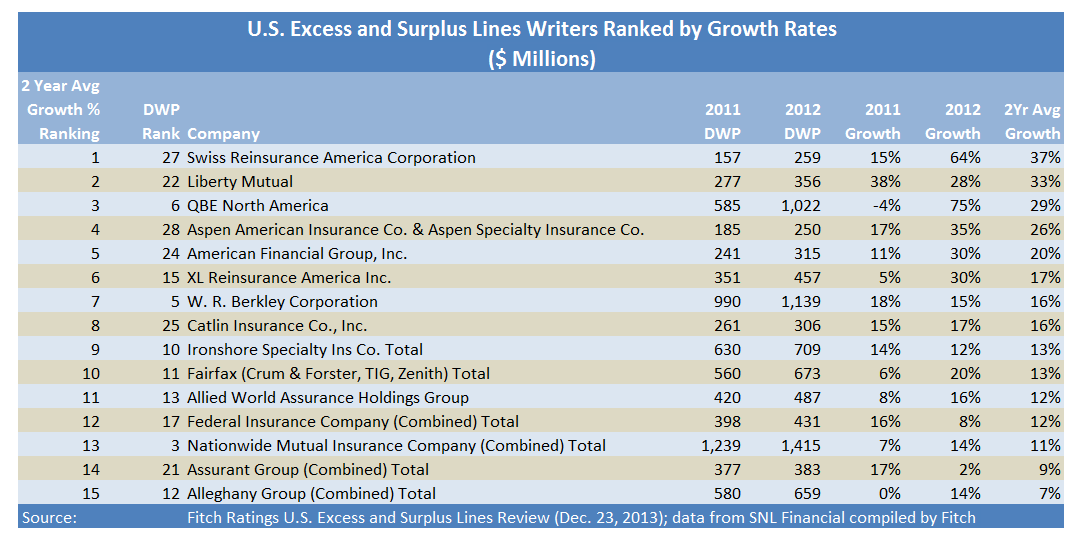

The report, published in Dec. 23, 2013 based on data for the 30 largest U.S. E&S insurers in 2012, shows that Swiss Reinsurance America Corp. and Liberty Mutual Insurance Co. were fastest growing E&S writers based on average annual direct premium growth for 2011 and 2012—posting average growth rates of 37 percent and 33 percent respectively.

Swiss Re jumped to 27th place in 2012 with $259 million in direct E&S premiums. Its 2010 premiums would have given it a last place ranking for that year when measured against premiums for other U.S. E&S writers in the 30-company group analyzed by Fitch using data from SNL Financial.

Liberty moved up six spots in the two-year period, leaping from a 28th place among the 30 carriers in 2010 to 22nd place in 2012 with $356 million in direct U.S. E&S premiums.

Only XL America had a bigger sprint—moving from 22nd place based on 2010 premiums to a 15th place ranking for 2012.

XL’s average annual growth rate of 17 percent for 2011 and 2012 was among the 10 fastest two-year growth rates calculated by Fitch.

Besides Swiss Reinsurance America and Liberty Mutual Insurance Co., three other groups—QBE North America (ranked sixth based on 2012 premium dollars), American Financial Group (ranked 24th), and Aspen Specialty (ranked 28th) grew faster.

QBE, with the third fastest two-year growth rate and a sixth-place ranking based on 2012 dollars of premium, was one of only three top-10 carriers (based on premium dollars) to show double-digit growth in the two-year period. W.R. Berkley and Ironshore were the other two.

Meanwhile, the two-year average growth rate for the biggest writer of U.S. E&S business—Lloyd’s of London—was only 4 percent, while second-place American International Group, had a 5 percent drop in premiums in 2012 after a flat year in 2011.

Fitch noted that standard carriers are refocusing on core risks and cutting back on risks typically covered in the E&S market, pointing out that U.S. E&S premiums for Travelers shrunk by 26 percent in 2011 and reported flat premium growth in 2012, compared with meaningful rate and exposure-related growth for the industry.

Travelers, ranked 26th among the 30 largest E&S carriers analyzed by Fitch with $282 million in direct U.S. E&S premiums. Travelers’ $380 million in U.S. E&S direct premiums for 2010 would have put it six spots higher—in 20th place—if the same 30-group were ranked based on their 2010 premiums.

Other companies to report lower premiums over the two-year period included Munich Reinsurance America and Argo Group US, according to tables included in the Fitch report.

Fitch also noted that Endurance grew tremendously during the soft market and shrunk in the more favorable pricing environment in 2012. Other companies to report significant growth during the soft pricing cycle include Catlin Insurance Co., Alterra Capital Group (sold contract binding authority division to Selective in August 2011, which makes up a portion of its E&S business, and acquired by Markel in 2013), and Allied World Assurance Holdings Group, Fitch said.

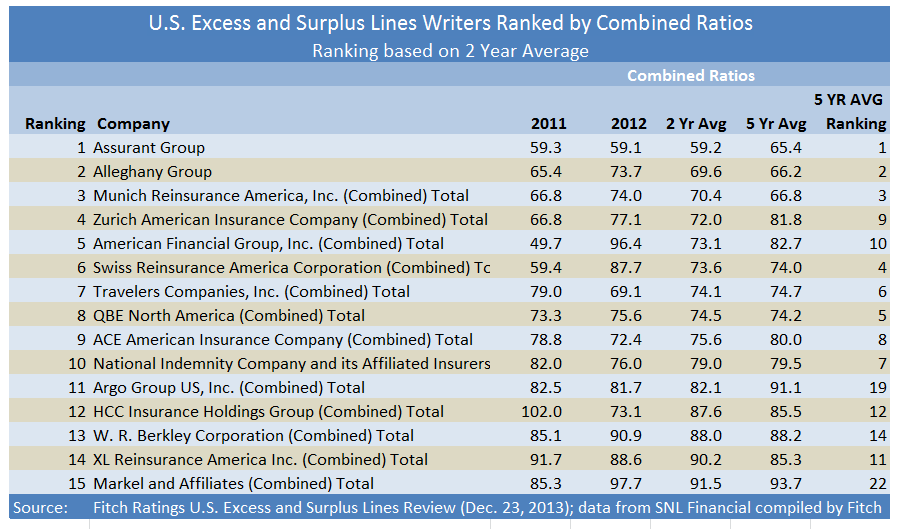

The Fitch report also includes an analysis of E&S combined ratios, and a ranking of carriers based on combined ratios shows consistency over the past five years. The carriers with the 10 lowest average combined ratios for the last two years also had the lowest in the last five. Assurant, Alleghany and Munich Re ranked first, second and third for both the two-year and five-year periods.

The full report, with premium and combined ratio data for all 30 E&S insurers analyzed by Fitch, is available on the Fitch web site at ‘www.fitchratings.com’ under ‘Insurance’ and ‘Research

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums