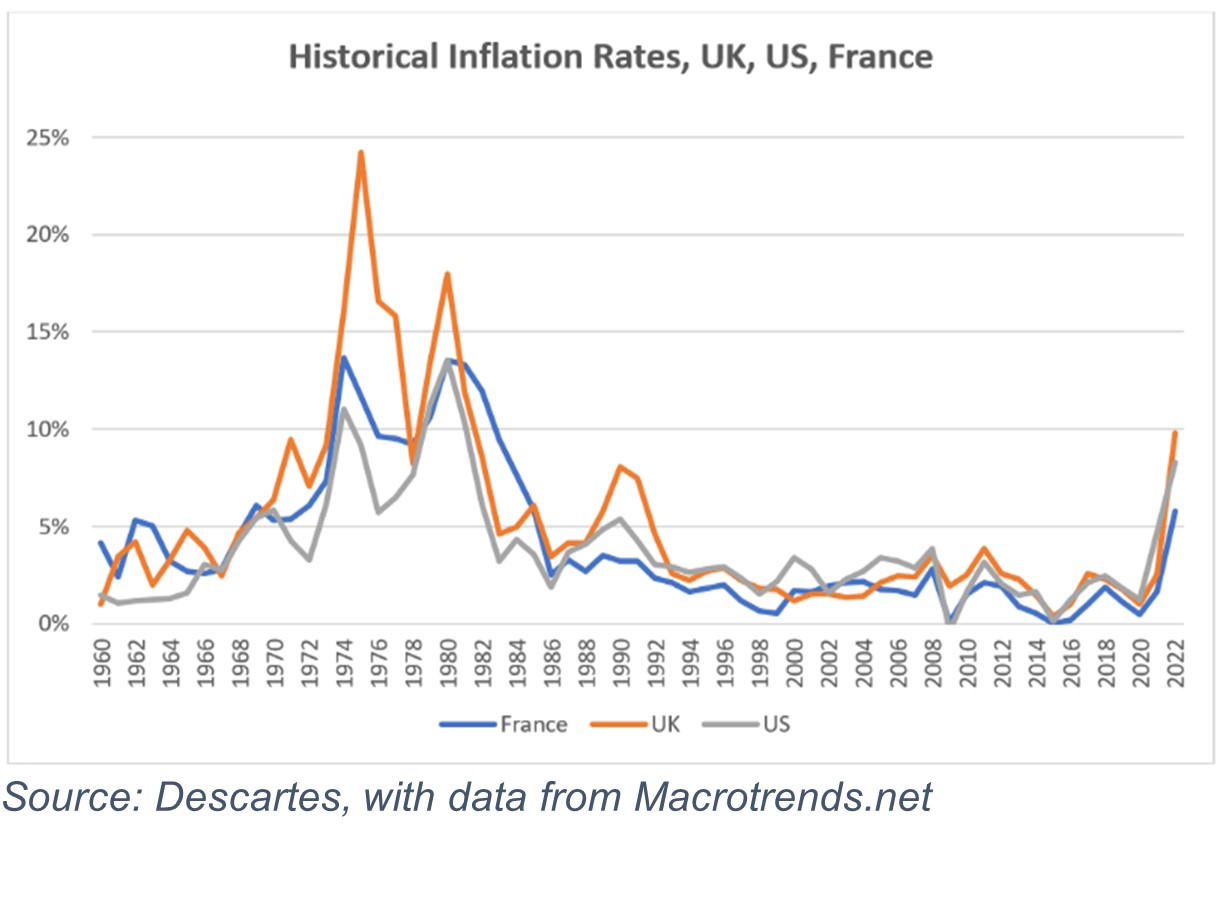

Annualized inflation in the U.S. topped 5 percent just once since 1981—until now.

Executive Summary

Inflation creates an extra source of uncertainty for P/C insurers setting loss reserves for incurred claims. And insureds face higher premium costs as inflation gets factored into insurer pricing calculations. Both impacts are gone when parametric insurance policies replace traditional offerings, Lockton's Peter Rapaciewicz reveals here. After a detailed discussion of inflations impacts on carriers and customers alike, Rapaciewicz explains that because financial loss is not directly relevant under a parametric insurance policy, neither premiums nor claims for such policies are impacted by inflation.In the UK, it exceeded 3 percent only rarely since 1992, and only ever by a fraction.

In France, the change in the cost of things has been even more stable during the past three decades, but inflation is back.

For the year ending Aug. 31, it was 8.3 percent, 9.8 percent and 5.8 percent, respectively, in those countries.

After decades of price stability, the return of inflation is causing a measure of havoc. While headlines herald a cost-of-living crisis, rising prices are having a complicated and sometimes convoluted impact in other areas, including the commercial insurance sector. Premium rates have been rising steadily for several years and still are on the increase, but little of the uplift so far has been intended to cover economic inflation. In some cases, inflation is only just now figuring into insurance pricing calculations after years of soft-market conditions.

{kind=link}