While more than 40 percent of insurers leave risk officer responsibilities to their chief executive officers or chief financial officers, just under 40 percent have a designated chief risk officer, according to a recent survey.

A.M. Best’s Spring 2016 Insurance Industry Survey, published in mid-July, revealed that 38.7 percent of the several hundred insurers responding have an actual CRO in the C-suite. Although the report didn’t indicate how the figure compares to prior years, it did note that presidents and CEOs take on CRO duties in 20.1 percent of companies surveyed. In addition, 23.2 percent of CFOs are managing the tasks of a CRO, the survey report said.

While the survey covers a broad cross-section of the industry—including life/health insurers in addition to property/casualty insurers—69 percent of respondents are from the P/C segment, and 95 percent of respondents are primary insurers, the report said.

The survey revealed information about other risk and compliance issues, including activities related to Own Risk and Solvency Assessments and perceived benefits of enterprise risk management.

For the insurers surveyed, the main ERM benefit has been that it drives a consistent view of risk throughout their organizations. Thirty-nine percent of respondents noted this impact. While just over one-fifth (20.5 percent) of the respondents said ERM is driving strategy and management effectiveness, only 10 percent cited the ORSA process in summarizing ERM impacts.

Drilling down on ORSA, the A.M. Best survey report said that 35.1 percent of respondents were obligated to prepare ORSA summary reports for their respective regulators (based on meeting a certain premium threshold). For the other 64.9 percent of insurers, only 15 percent that were not obligated to prepare ORSA reports did so voluntarily, the survey revealed.

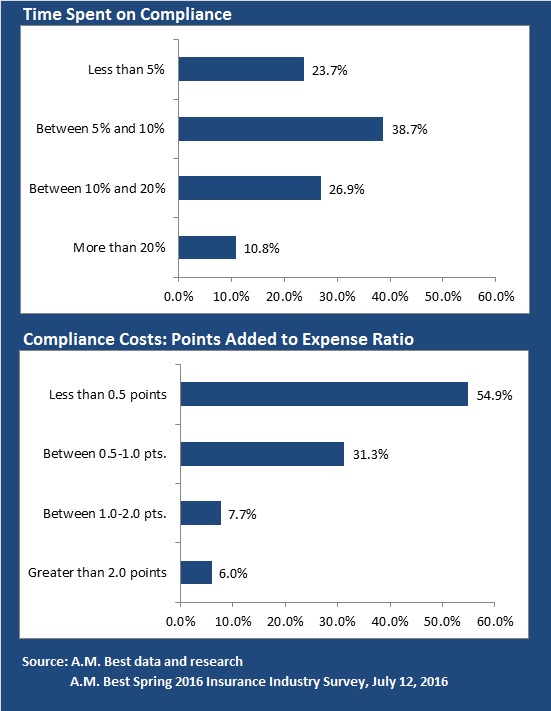

Whether they were required to submit ORSAs or not, regulation and compliance is taking a toll in terms of time devoted to compliance activities and increased costs.

Almost two-thirds of respondents (63 percent) said they saw compliance costs grow by 10 percent or more over the five-year span ending in 2015, with nearly one-quarter of all respondents (23.8 percent) pegging compliance-cost growth at 25 percent or more. Only about 13 percent saw no change in these costs over the period.

Still, most (54.9 percent) said that compliance added less than a half point to their company’s overall combined ratio in 2015. But in terms of hours spent on compliance, more than one-third said that their designated risk officers spent at least 10 percent of their time on compliance issues.

While compliance with regulations like ORSA hasn’t been a big benefit of insurers’ ERM efforts, 18.5 percent of respondents said the early identification of emerging risks was a significant impact of ERM developments.

The A.M. Best survey, published on July 19, also queried insurers about targeted returns on equity (with nearly three-quarters targeting ROEs of 10 percent or lower), the stability of economic conditions, looming threats, capital management activities, cyber risk management, reinsurance trends and drivers of success, among other topics.

Selecting among factors that will be key drivers of success in the next 24 months, ERM strategy ranked near the bottom, with only 13.4 percent of carriers identifying it as a potential key to organizational success. Only mergers and acquisitions activity and international expansion ranked lower, while efforts to upgrade information systems and improve customer experience were seen as top success drivers (each selected by roughly 50 percent of respondents).

Global Commercial Insurance Rates Keep Falling; Down 8 Quarters in a Row

Global Commercial Insurance Rates Keep Falling; Down 8 Quarters in a Row  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal

Mapfre to Acquire Safety Insurance in $1.5B in Cash Deal  Deja Vu as Berkley Calls Out MGUs During Quarterly Call

Deja Vu as Berkley Calls Out MGUs During Quarterly Call