Twenty years ago, on Jan. 17, 1994, a previously unknown fault ruptured nine miles beneath Northridge in the San Fernando Valley.

Executive Summary

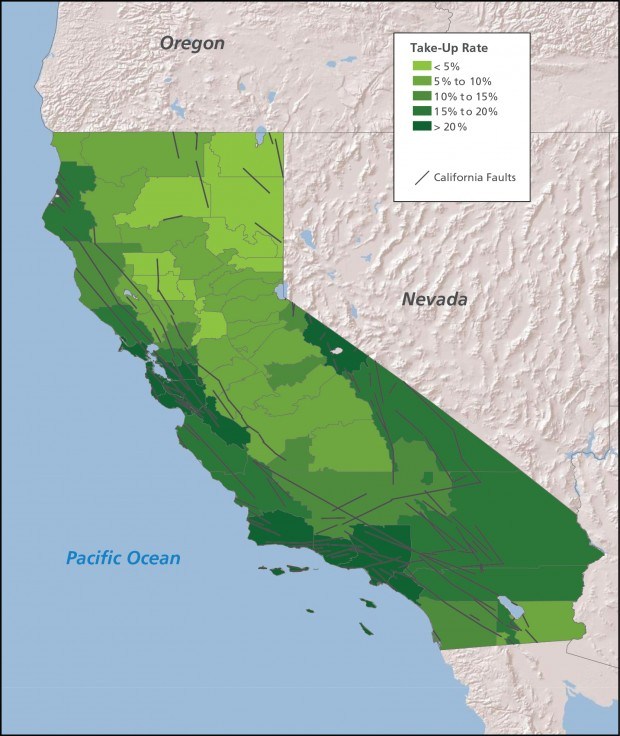

For a California earthquake that causes $20 billion of residential property damage, insurance recoveries would amount to less than $2 billion, according to AIR Worldwide. The low level of coverage is "a systemic failure," writes AIR COO Bill Churney, who argues that models now analyze detailed information on hazards like response to earthquake stresses and that the quality of exposure data is much more adequate for risk assessment than in 1994, when Northridge occurred.With a magnitude of 6.7 and an epicenter just 20 miles northwest of downtown Los Angeles, the earthquake produced the largest ground motions ever recorded in an urban environment in the United States, heavily damaging more than 40,000 structures across several counties.

Insurance companies paid out a record $12.5 billion in claims—substantially more than the total amount of earthquake insurance premiums collected during the previous several decades, with the obvious implication that the industry had significantly underestimated the risk.

The effect on homeowners insurance in California was immediate and radical. Because companies selling homeowners insurance in California were required to offer earthquake insurance as well, many insurers chose not to bear the highly uncertain risk and stopped writing new policies altogether.