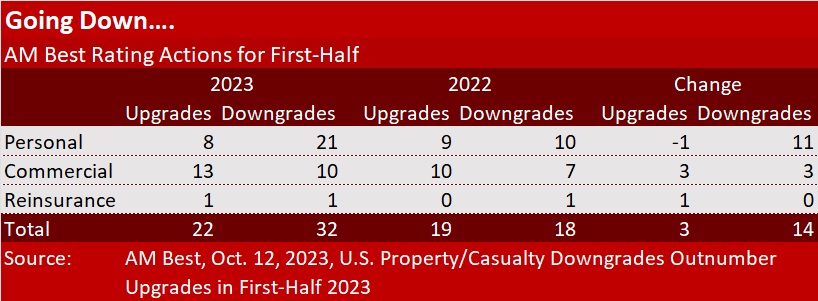

The number of rated property/casualty personal lines insurers that had their credit ratings downgraded by AM Best more than doubled to 21 in the first-half of 2023, compared to 10 in first-half 2022.

Additional downgrades of 10 commercial insurers and one reinsurer brought the P/C insurance industry total to 32 for this year’s first half, compared to 18 in total for last year’s first half, the rating agency said in a report released in mid-October.

Together, the P/C downgrades accounted for 9.1 percent of all AM Best’s ratings actions taken during the first half of this year. In contrast, for first-half 2022, downgrades accounted for 5.2 percent of the firm’s rating actions.

In addition, Best reported that the number of P/C ratings placed under review more than doubled in the first half of 2023 and made up 6.3 percent of total rating actions.

Noting that personal auto insurers accounted for 11 of the 21 personal lines downgrades, AM Best characterized the prospect of a near-term return to underwriting profitability as “unlikely” for personal auto carriers. Personal lines downgrades also reflected weather-driven deterioration in operating performance.

Weather, rising claims frequency and severity and supply chain issues dented both operating results and capital levels of personal lines insurers, the report said.

On the commercial side, where upgrades continue to outpace downgrades this year, commercial casualty accounted for five of the 10 downgrades, AM Best said, pointing to social inflation as a factor.

Across segments, more than one third of downgrades—38.7 percent—were attributable to declining operating results; weakened balanced sheets accounted for 22.6 percent of downgrades. (Note: Other downgrades were attributable to multiple building blocks of rating assessments, all of which included balance sheet strength, Best said.)

In terms of carrier rating outlooks, the percentage of negative outlooks doubled over the last six months—to 9.9 percent as of June 30, 2023 from 5.4 percent at year-end 2022.

Looking ahead, AM Best said, “Carriers that are slow to address challenges or do not have the means, expertise, or technological capabilities to keep pace with changes in the environment will likely face ratings pressure,” referring to personal lines insurers. While commercial carriers face headwinds, the segment remains solidly capitalized with “conservative investment portfolios, sound reserve positions and enhanced risk management discipline,” the report said.

The number of ratings under review as of June 30—18 rating units—isn’t much different than the year-end total of 16.

A few days before AM Best published its report on upgrades and downgrades, the rating agency announced that it was placing another carrier’s ratings under review, with the Maui wildfires contributing to the rating status of the company, Universal North America Insurance Company (UNAIC) (Arlington, TX).

AM Best placed UNAIC’s financial strength rating of B+ (Good) and the long-term issuer credit Rating of “bbb-” (Good) under review with negative implications, noting a 12 percent drop in its policyholder surplus (and corresponding decline in overall risk-adjusted capitalization), owing to severe convective storms through the second quarter, and a further surplus decline because of the company’s exposure to the Hawaiian fires.

Prior to being placed under review, UNAIC’s ratings had a negative outlook due to continued pressure on the balance sheet strength and operating performance assessments.

Historically, the ultimate parent, Universal Group, Inc., has provided support and remains committed to adequately capitalizing the company, AM Best said, adding that the ratings will remain under review until AM Best can fully analyze the company’s proposed capital management strategy.

In the absence of an adequate capital management plan that is supportive, the ratings will most likely be downgraded, AM Best said in the UNAIC announcement.

Source: AM Best

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention  Soft P/C Market May Be Shallower Than Previous Cycles: Swiss Re

Soft P/C Market May Be Shallower Than Previous Cycles: Swiss Re  Why Consistency Beats Creativity in Insurance Marketing

Why Consistency Beats Creativity in Insurance Marketing  Default Speed Limit in Iowa Changes from 55 to 60MPH

Default Speed Limit in Iowa Changes from 55 to 60MPH