In a year when cyber insurers notched the third-lowest industrywide loss ratio since 2015, and cyber premiums vaulted to $7.2 billion, a premium ranking shows two carriers growing more than 150 percent to landing in prominent top-10 spots.

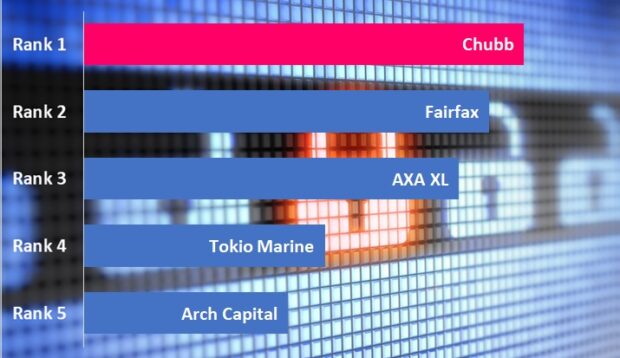

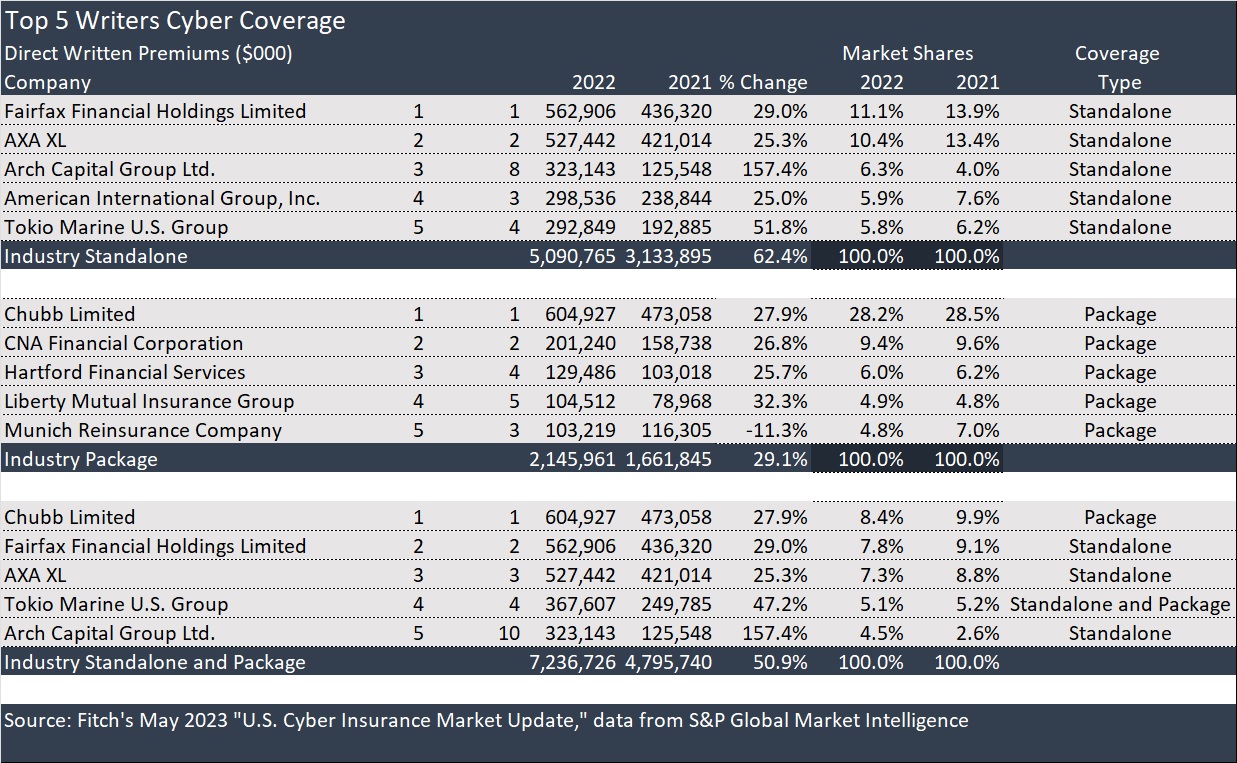

Fitch compiled and analyzed premium and claims information included in the Cybersecurity and Identity Theft Insurance Coverage Supplement of statutory financial data in a new report, “U.S. Cyber Insurance Market Update,” published late last week. A bar graph in the Fitch report displays the carriers in rank order based on levels of direct cyber premiums written by insurer—for both standalone policies and package policies combined.

The graph shows Arch Capital’s 157 percent jump to $323.1 million in direct cyber insurance premiums putting it in fifth place overall. Nationwide, with $240.1 million in standalone cyber policies ranks eighth on a combined ranking, according to Fitch. In 2021, Nationwide wrote under $9 million in standalone cyber premiums, according to the Fitch report.

The Fitch report also displays top 10 rankings separately for standalone and package writers. Below, Carrier Management editors have extracted the top 5 for standalone policies and for package policies, adding them together for a top 5 ranking of cyber insurers overall (last section of the table).

Although CNA is the second largest insurer for cyber package policies, Nationwide’s sprint up the ranks of standalone writers, pushed CNA out of the top 10 cyber insurers overall based on 2022 direct premiums for both type of policies.

Making up just 1 percent of U.S. property/casualty insurance premiums in 2022, Fitch reports that cyber insurance is the fastest growing market segment in U.S. P/C industry with direct written premiums up nearly 51 percent in 2022. The increase followed at 73 percent jump in direct written premiums in 2021. In both years, standalone premium growth outpaced package policy growth. Standalone cyber premiums for the industry grew 62 percent in 2022 (and 92 percent in 2021), while package premiums grew just over 29 percent last year.

With claims trends improving, and two years of hard market pricing helping to push the overall direct loss ratios down in 2022, “Fitch expects rates to flatten further, which may lead to a negative shift in pricing trends, similar to current trends in directors and officers liability coverage following a previous sharp rise in rates,” the rating agency said in a media statement about the report.

For standalone cyber insurance, the statutory direct loss ratio (including defense and containment cost), dropped almost 25 points to 43 in 2022, compared to 68 in 2021.

The Fitch report shows direct loss ratios in 2022 and 2021 for each of the top 10 carriers, revealing that American International Group showed the biggest individual carrier improvement—falling to 47.8 in 2022 from 131.8 in 2021. (AIG was the only carrier in the top 10 to report a standalone cyber loss ratio over 100 in either year, according to the information in the Fitch report.)

Although the financial data in the statutory supplement does not provide a complete picture of underwriting results—it is missing underwriting expenses and adjusting costs—Fitch believes the loss ratio improvement indicates a return to underwriting profitability for the cyber segment in 2022.

Comparing average supplement loss ratios for 2015-2022 to average loss ratios for other lines over the same eight-year period, Fitch reported that cyber came in 7 points lower than workers compensation—the next most profitable line over the period. (According to Fitch, 2015 is the first year in which the cyber supplement data became available.) The cyber loss ratios from one year to the next are more volatile than other lines, however. The standard deviation of the cyber loss ratios, a measure of variability, is nearly triple the standard deviation of workers comp loss ratios, according to Fitch’s calculations.

While a graph in the report that tracks premiums and loss ratios in a single visual representation shows the steep climbs in premiums in the last three years corresponded to loss ratio plummeting from a high of 72 in 2020, Fitch notes that the underwriting performance improvement is also tied to moderating claims trends, including lower ransomware incident costs and a higher proportion of ransomware incidents without payment.

Using the cyber supplement data to confirm those trends reported by cyber industry expert Coveware, Inc., Fitch found that cyber claims reported to P/C insurers writing standalone coverage rose 27 percent over the last two years. With premiums rising faster, frequency dropped to 5.3 percent in 2022 from 6.9 percent in 2021.

Still, “the claims environment remains highly fluid, given the rapid pace of technological and economic change, such that recent relative claims stability may prove short lived,” the Fitch report notes.

Cyber Market Less Concentrated

Fitch reports that a total of 25 organizations wrote more than $100 million of direct cyber premiums written in 2022, and 34 wrote more than $25 million.

Established insurers in the segment, including Chubb, AXA XL and AIG continued to grow, but more rapid growth among several companies drove a shift in market share rankings and reduced market concentration in the last few years. At year-end 2022, the top 10 U.S. cyber writers accounted for just over half of industry direct written premiums, while just four years ago, the top 10 commanded 69 percent in 2019.

In addition to Arch Capital and Nationwide, Sompo Group and Swiss Re America saw standalone cyber premiums grow more than the overall market.

On the package side, Zurich American reported a four-fold jump in premiums, landing the carrier in 10th place on a ranking of package providers In 2022, while fifth-ranked Munich Re reported only drop in volume (11.3 percent) among the package players.

Beazley and BCS Insurance, which appeared on prior top-10 and top-15 cyber rankings compiled by Fitch and AM Best in 2018-2020, are not listed among the top writers in the Fitch report published last week.

Berry Producer Driscoll’s Sued Over Alleged Use of Forever Chemicals

Berry Producer Driscoll’s Sued Over Alleged Use of Forever Chemicals  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs