The federal flood insurance program is on a course to continue falling deeper in debt, even when there is no catastrophic storm like Katrina or Harvey.

The federal flood insurance program is on a course to continue falling deeper in debt, even when there is no catastrophic storm like Katrina or Harvey.

The National Flood Insurance Program (NFIP) is currently on a path that will lead to a shortfall of $1.4 billion because its method for setting premiums has underestimated how much its claims will cost by about $1.1 billion and also because legislated surcharges are about $300 million shy of what’s needed to cover premium discounts given to certain properties, according to the Congressional Budget Office (CBO) report, National Flood Insurance Program Financial Soundness and Affordability.

Also, according to part of the analysis that could draw political interest along geographic lines, under the NFIP’s current structure, policyholders living in inland counties are subsidizing policyholders in coastal counties, particularly in southeastern and Gulf Coast states.

The CBO report was written before Hurricane Harvey hit Texas and Louisiana. It was issued as Congress is returning to Washington to consider reauthorization of the flood program along with billions in disaster aid for victims of Hurricane Harvey

For this report, CBO analyzed roughly 5 million policies in effect on August 31, 2016, which it said approximate the policies currently in place. CBO’s estimate of expected claims accounts for low-probability, high-cost events, such as Hurricane Harvey. As a result, CBO says its estimate is “probably greater than actual costs would be in a typical year, although lower than costs could be in the aftermath of a catastrophic storm” such as Harvey.

CBO estimates that the NFIP faces $5.7 billion a year in costs while bringing in only about $4.3 billion in revenues. NFIP collects about $3.3 in premiums and about $1 billion in surcharges and fees a year.

Using commercially available computer predictive models, CBO estimates expected actual claims costs to be about $3.7 billion a year, which is $1.1 billion more than the program’s administrator, the Federal Emergency Management Agency (FEMA), projects using its own method of analyzing historical data.

Of the total costs of $5.7 billion in CBO’s analysis, $3.7 billion covers claims, $1.1 billion goes to private insurers and brokers for their selling and servicing of policies, about $200 million is for salaries, about $200 million is for flood plain mapping, $200 million is for mitigation grants, and $300 million is for interest payments on the $24.6 billion debt NFIP owes the Treasury.

On top of the claims cost discrepancy, CBO said the rest of the NFIP’s $1.4 billion shortfall is due to a $300 million gap between discounted rates for certain policies and the money from surcharges created to help cover the costs of those discounts. The discounts are mainly for properties built before the development of flood insurance rate maps (FIRMs) and are meant to prevent hardship on homeowners that might cause some to not buy coverage.

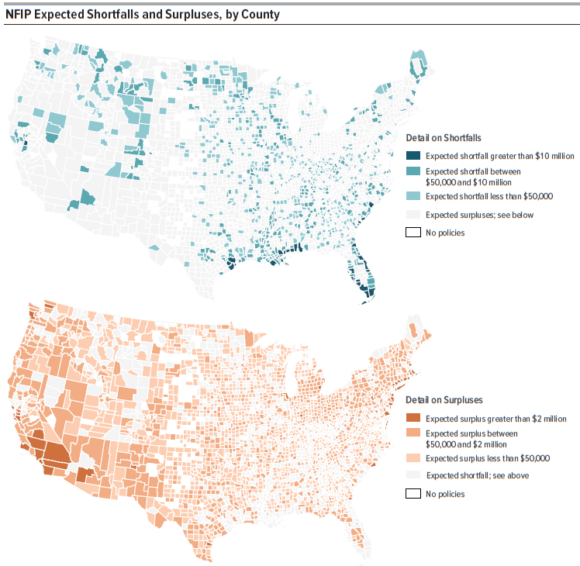

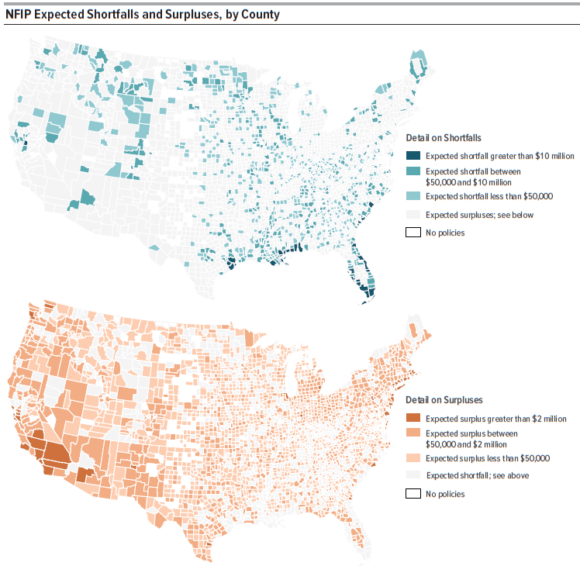

Coastal Counties

CBO examined the contributions of coastal and inland counties to the $1.4 billion difference between NFIP’s total expected costs and premiums and concluded that the overall NFIP shortfall is largely caused by underpricing in coastal counties, which account for three-quarters of all NFIP policies nationwide.

“The agency estimates that the shortfall for the NFIP program as a whole stems largely from premiums falling short of expected costs in coastal counties, rather than in inland counties,” CBO says. “Although some coastal counties generated surpluses and some inland counties contributed to the aggregate shortfall, on the whole, coastal counties generated a shortfall that was greater than the aggregate shortfall, and inland counties generated a small surplus.”

CBO says the difference between coastal and inland counties is influenced by two factors: subsidies built into the NFIP and FEMA’s rate-setting system, both of which favor coastal policyholders.

“The result is that most policyholders whose property is at risk of wave damage from storm surges do not pay premiums that cover their expected costs. Instead, the additional expected costs from wave damage are spread broadly among the NFIP’s policyholders, resulting in a cross-subsidy from inland counties (on average) to coastal counties: That is, some of the expected costs associated with coastal policies are covered by higher premiums paid by policyholders in inland counties,” the study says.

The fact that premiums on policies for most homes in coastal areas do not cover the expected cost of wave damage from storm surges is important. Storm surge, the report notes, is a significant contributor to flood losses. Over the past 35 years, hurricane-related storm surges have been responsible for 37 percent of claims, followed by inland flooding primarily from rivers, lakes and ponds at 36 percent. Hurricane-related rain (16 percent), tropical storms (5 percent), and nor’easter coastal storms that typically affect the northeastern and mid-Atlantic states (2 percent).

The NFIP had a shortfall in about one-fourth of all 2,984 counties that CBO analyzed; the program had a surplus in the rest of the counties. For most counties, the difference between premiums and expected costs was small. The net shortfall measured over all coastal counties was $1.5 billion, whereas the net surplus measured over all inland counties was $200 million.

But CBO also found that out of 823 counties with a total of $2 billion in shortfall, 33 of them showed a shortfall of more than $10 million, or nearly 90 percent of the $2 billion total. These 33 counties, which are located mostly along the southeast coast and the Gulf of Mexico, had both large numbers of policies (41 percent of all NFIP policies) and high average shortfalls per policy ($840, compared with $220 for the 790 counties with smaller shortfalls).

The surpluses also were geographically concentrated, although not as much as the shortfalls. CBO estimates that 59 counties with surpluses of more than $2 million accounted for roughly 60 percent of the $600 million total from all 2,161 counties with surpluses. Those 59 counties, mainly located along the northeast and west coasts, contained 16 percent of all NFIP policies. Their average surplus per policy was $480 compared with $280 for the roughly 2,100 counties with smaller surpluses.

Affordability Assessment

CBO also assessed the NFIP’s affordability for policyholders. Comparing premiums with household income from census data, it found:

- The median annual premium for residential NFIP coverage is $520.

- Most of the premiums—specifically, the central two-thirds of the distribution around the median of $520—are between $420 and $1,330.

- The median value of the ratios of census tracts’ median premium to median household income is 0.8 percent; the central two-thirds of the ratios fell in the range of 0.5 percent to 1.5 percent.

- Premiums differed somewhat by type of residence. The median premium for condominiums (one-fourth of the total) was about 15 percent lower than the median premium for single-family non-condominium homes ($440 per year versus $520 per year). Those differences reflect generally lesser coverage for condominiums.

- Within the subset of single-family non-condominium residences, premiums tended to be significantly lower for primary than for non-primary residences. The median annual premium was $450 for primary single-family residences (56 percent of all residential policies); it was $740 for non-primary single-family residences (19 percent of all residential policies). Of that difference of $290, $225 can be attributed to lower fees for primary residences as the surcharge to help cover the costs of discounted rates (primarily for pre-FIRM properties) is $25 for policies that cover primary homes and $250 for policies that cover non-primary homes and non-residential properties.

Authority Expires; Harvey Aid

Insured losses, including for flooding, from Hurricane Harvey are still being tabulated. Data analytics firm CoreLogic has projected home flood insurance losses from Harvey running between $6.5 billion and $9.5 billion. Hurricane Katrina resulted in more than $15 billion in flood insurance losses in Louisiana and Mississippi.

The current authorization for the NFIP expires in less than four weeks on Sept. 30. If Congress does not reauthorize it by that date, it will still be able to pay claims from funds on hand, but it will not be able to borrow additional funds, renew policies or issue new ones.

Congressional lawmakers returning to Washington this week are not in agreement on what to do about the NFIP. Some have said Harvey is a reason to press for program reforms now while others have called for a straight reauthorization, leaving reforms for another day.

Under current law, FEMA can borrow up to $30.4 billion from the Treasury to operate the NFIP. The agency owes the Treasury $24.6 billion, leaving $5.8 billion in remaining borrowing authority. The program was forced to borrow heavily to pay claims for Hurricanes Katrina, Rita, Wilma and Sandy. It also borrowed $1.6 billion in January 2017.

Lawmakers also have President Trump’s request for close to $8 billion in aid for victims of Harvey to consider.

Reform Approaches

The CBO report closes with a discussion of a dozen approaches that lawmakers could consider to “make the program more solvent, align premiums with risks, or keep rates low.” They include:

- Improve solvency by increasing premium income from policyholders in general, reducing the use of discounted rates, or increasing the share of costs borne by certain categories of policyholders or by taxpayers generally;

- Better align premiums with risks by reducing the use of subsidies, including discounted rates and cross-subsidies (in which some policyholders are charged rates that are higher than their expected claims so that other policyholders can pay rates that are lower than their expected claims), or by adjusting premiums to better reflect underlying risk factors;

- Keep costs low for some policyholders (perhaps while raising them for others) by targeting subsidies to low-income policyholders, shifting costs to taxpayers, or adjusting premiums to reflect the value of insured properties.

Source: Congressional Budget Office (CBO) report, National Flood Insurance Program Financial Soundness and Affordability

*This story appeared previously in our sister publication Insurance Journal.

Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study  UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment