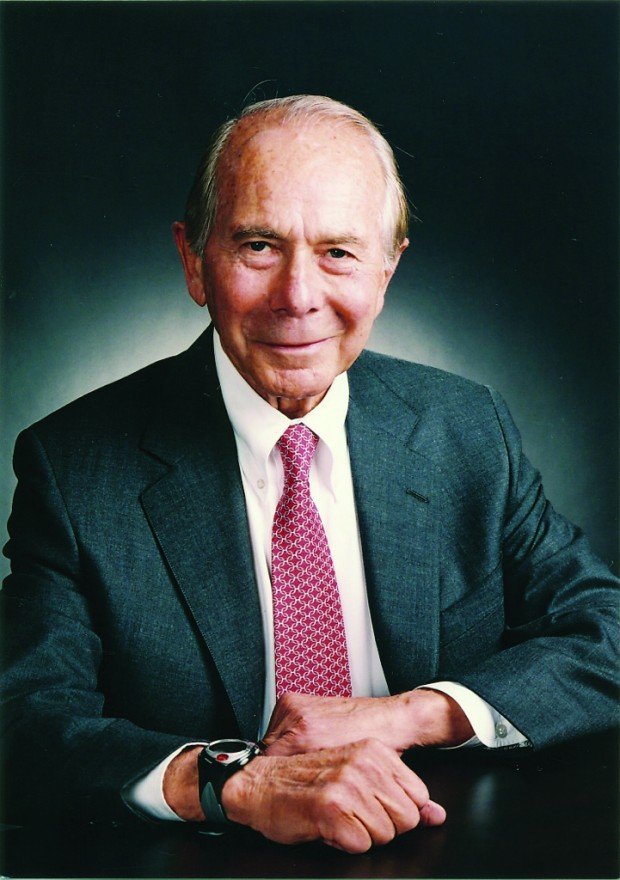

Since his ouster from American International Group Inc. in 2005, Maurice “Hank” Greenberg has been quietly building an insurance and investment conglomerate that people close to him describe as a mini version of Warren Buffett’s Berkshire Hathaway Inc.

Greenberg’s $4.4 billion acquisition, announced Monday, of health insurance claims processor MultiPlan Inc. is by far the largest in a series of investments carried out through the private investments arm of his insurance and investment firm, C.V. Starr & Co., which was set up by AIG founder Cornelius Vander Starr in 1943.

The MultiPlan deal could be the clearest sign yet of how Greenberg, 88, has been working on a Wall Street comeback after spending the last few years dealing with a multitude of lawsuits and investigations while suffering huge losses in the value of his AIG holdings as the insurance giant tottered during the financial crisis.

Although Greenberg’s closely held company does not disclose financial details, people familiar with the matter said its private investments arm, Starr Investment Holdings LLC, had more than $3 billion in assets under management. It is tiny compared with Berkshire Hathaway, which has a market value of $283 billion.

In the MultiPlan deal, Greenberg deployed some of the same tactics as Buffett – using cash flow from a set of operating companies and assets as well as his relationships to pull off a large deal.

“We have a rapidly growing insurance arm, we have a real estate business, and we also have a unit that helps Chinese companies invest in the U.S.,” Greenberg said in an interview. “We are private, we don’t advertise what we are doing, and we will stay private,” added Greenberg, who described the private investments arm as a significant driver of earnings.

Greenberg, who – according to Forbes – had a net worth of $3.2 billion around the time he was ousted as AIG boss, last year told talk show host Charlie Rose he had lost around 90 percent of his wealth as a result of AIG’s collapse. AIG shares are still trading at a tiny fraction of their pre-crisis levels.

Leading Starr Investment Holdings is Geoff Clark, already a veteran private equity dealmaker at the age of 41.

After co-founding Goldman Sachs Group Inc.’s private equity group in 1996 and being its co-head until 2004, Clark joined Starr in 2007, at a time when it invested in private equity funds but also made direct private equity investments.

He led Starr Investment Holdings as it launched as a dedicated private investments business in 2012 and adopted an investment horizon that can go beyond the typical five-to-seven-year period that buyout firms tend to hold companies before selling them or doing an initial public offering.

Rising Starr

Rather than manage a traditional private equity fund that raises money from investors and then decides how to invest it, Starr Investment Holdings reaches out to investors on a deal-by-deal basis to seek their participation.

Greenberg brought Swiss alternative asset manager Partners Group Holding AG and three other investors into the MultiPlan deal.

The identity of the other investors, and information about the size of their stakes, was not disclosed but a person familiar with the deal said they included Bill Gross’ Pacific Investment Management Co., the world’s largest bond fund manager. A Pimco spokesman did not respond to a request for comment.

“Mr Greenberg was very involved on the Starr side,” Joel Schwartz, Partners Group managing director, said in an interview. “We met with him during the deal, but we really did the transaction with Starr Investment Holdings.”

Last year, Starr Investment Holdings brought in Partners Group as a shareholder in home decoration retailer Garden Ridge, a portfolio company of private equity firm AEA Investors LP. Starr, which was already a Garden Ridge investor, invited Partners Group into the deal when some of the other shareholders decided to exit.

Greenberg’s links to the insurance world proved crucial to the MultiPlan deal, both in terms of relationships and also understanding MultiPlan’s business and clientele, people who worked on the deal said.

MultiPlan Chief Executive Mark Tabak, who Starr and Partners Group plan to keep at the company’s helm, worked for Greenberg between 1993 and 1996 as president of AIG Managed Care.

“We have known each other for a long time. He was a very key player, we probably would not have done (the MultiPlan deal) without him and he would not have done it without us,” Greenberg said of Tabak.

MultiPlan is the oldest and largest provider of cost management solutions for the U.S. healthcare industry. The company’s cash flow has increased 50 percent since 2010 and Moody’s Investors Service said this week that MultiPlan continues to be in a market with high barriers to entry and solid organic growth.

Greenberg had served as AIG chief executive for almost four decades when he was forced to step down amid an investigation by Eliot Spitzer, then the New York Attorney General, into the company’s business practices. The following year, the insurer paid $1.64 billion to settle federal and state probes.

Greenberg still faces some New York state charges over allegedly sham transactions, which he vehemently denies doing. Last year, he sued Spitzer for defamation as the former New York state governor was trying to stage his own comeback.

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums