Opportunity is real. An interesting result of our world economy and the rise in technology is that small businesses are on the rise, fueled by growing opportunities. Small businesses are now enabled by the offering of capabilities that used to be difficult and necessary but are now available as simple services or those which make any business run smoothly.

Whether you have a fashion business on your small-town square, a bookstore operating out of your living room in the suburbs, or a food kiosk in an urban food court, you’re likely doing what you couldn’t do yesterday because you’ve been enabled by technologies that weren’t widely available yesterday.

Think of the resources that small retailers have at their fingertips now to make their business operate at a higher level.

Shipping. UPS, FedEx, and USPS have made labeling, shipping, and postage from your location, easier than ever before.

Warehousing. Today’s small vendor has stock and ship options, such as Amazon’s warehouse program, where storage and fulfillment are done by Amazon.

Transactions. Cash was preferred until companies like Square paired simple interfaces with mobile convenience and packaged their services as quick-start, anywhere-ready.

The lesson is applicable across all industries. Off-loading necessary operational constraints can give businesses a great deal of their freedom back that will benefit necessary operations and services. The savings of time, finances, and headaches can compensate for non-negotiable price and demand issues. Most small businesses would not survive without partner technologies.

Today’s innovation is one part inspiration and one part letting go of the past and what you no longer need to do.

What is innovation, anyway?

In Majesco’s recent Thought Leadership report, 10 Trends Shaping the Future of Insurance, we find that 2024’s strategic initiatives drive growth, but also reflect the need for innovation. They point to the fact that innovation needs to focus on both today’s operations while creating tomorrow’s – which will likely be very different. Innovation includes exciting forward-facing technologies and creative day-to-day operation models, like underwriting transformation, that enable the company to move in new directions. The greatest innovations are those that meet both today and the future strategic goals possible.

What does innovation mean to your company, and more specifically, how are you executing as compared to your competitors?

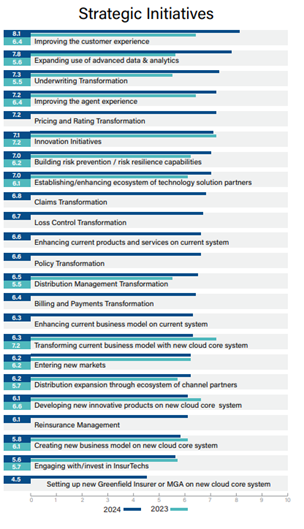

Strategic Initiatives for 2024

In the May 2023 BCG report, Most Innovative Companies 2023: Reaching New Heights in Uncertain Times, it notes that for the third straight year, companies that both prioritize innovation and make sure that they are ready to act are widening the gap over less capable competitors. The report highlights that Leaders at these firms are consistently delivering new products, entering new markets, and establishing new revenue streams. The Laggards struggle to make headway beyond incremental improvements. The report notes that despite global economic uncertainty, innovation rose as a top corporate priority in 2023, with 79% of companies ranking it among their top three goals.[i]

In the August 2023 Best’s Special Report, the ability to execute in a fast-changing marketplace is highlighted by the innovation ratings assessment across five ratings: Leader, Prominent, Significant, Moderate, and Minimal – showed little positive progress from 2021 to 2023. With only 5% for P&C and 4% for L&A assessed as Leader or Prominent and 19% for P&C and 23% for L&A with a Significant assessment, the result is that nearly 75% of the industry is not making the progress needed to meet the growing and intensifying challenges and demands.

This is consistent with our 2023 Strategic Priorities research, with insurers placing innovation as a top 10 strategic priority and Leaders outpacing Followers and Laggards with growing gaps due to the lack of focus on both operational and strategic innovation.

Given the market challenges and changes during 2023, we are seeing a shift in our 2024 Strategic Priorities research as compared to the 2023 results shown below in Figure 1. Within the top 12, 5 are new areas of focus and the other 7 have seen significant shifts in ranking, reflecting the impact of the market changes and macro-economic challenges.

Rising to the top are those areas that have a direct influence or impact on profitability (underwriting transformation, pricing & rating transformation, claims transformation), growth and loyalty (customer experience, agent experience, enhancing current products and services on current system), risk management (risk prevention/risk resilience capabilities, loss control transformation) and innovation (innovation, ecosystem of solution partners).

Figure 1: Insurers’ strategic initiatives, 2024 vs 2023

However, due to a combination of factors, many insurers still operate with traditional, historical operational practices and technology, keeping them in a legacy environment that does not allow them to adapt or keep pace with changes in the market, customers, and risk. In particular, the slow, steady 3%-4% of DWP technology investment is incremental at best and insufficient to meet the pace of change and demands in today’s marketplace.

Insurers need to find the right formula for profitable growth by not only doubling down on investing in a new business model and technology but also by finding technologies that relieve the burdens of operations while improving the growth potential. If not, the gaps we are seeing between Leaders versus Followers and Laggards and the Innovation Rating gaps will continue to increase, putting many carriers in an increasingly difficult position, one that may be unrecoverable.

Trends for 2024

Strategic discussions on how insurers will prepare for and manage the changes needed in their business models, products, channels, and technology are more important now than ever. To improve operations, insurers must:

- Address and replace legacy operational and technology debt.

- Enable innovation, product line, and business expansion.

- Improve ease of doing business and expand channels for better retention and sales.

Below are three trends that Majesco identified as reflecting those areas of priority insurers should consider and focus on to create a path forward for scalable and sustainable change.

Trend 1: Legacy Debt Comes Home to Roost – Deteriorating the Business

Over the last 10-15 years, we have seen a shift in core systems, both in terms of technology and business capabilities, from the monolithic core on mainframes to on-premise modern core components that were the start of modernization and transformation programs. But most of these programs were painful and expensive, often running over many years and costing tens to hundreds of millions of dollars due to the highly customized, on-premise implementations that have been difficult or nearly impossible to upgrade. In addition, too often the older systems that were to be replaced remained in place due to the cost of converting to the new system.

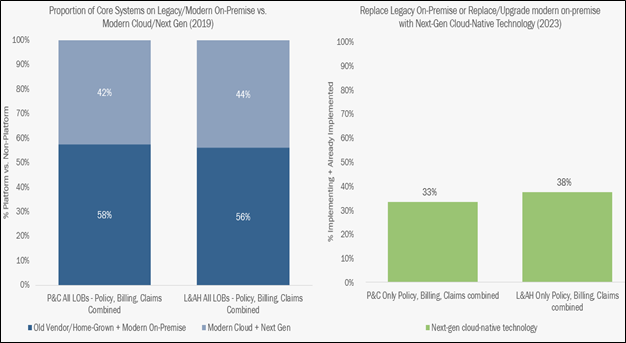

Figure 2: Proportion of Core Systems on Legacy/Modern On-Premise vs. Modern Cloud/Next Gen

The result has been that legacy never went away, remaining the same or slightly growing. In our Core Systems Report based on a 2019 survey to insurers, both P&C and L&AH had 56%-58% of their core systems as non-platform, meaning they were old vendor, home-grown or modern on-premise, as shown in Figure 2 above. In our current survey conducted in Q4 2023, only 38% and 33% of L&AH-Only and P&C-Only carriers, respectively, said they were implementing or had implemented replacements or upgrades of legacy or modern on-premise core systems to next-gen cloud-native technology, as seen in Figure 2, reflecting no movement or slight decline in dealing with the core as compared to 4 years ago.

With retirements increasing and the loss of institutional knowledge and skills, legacy debt is becoming a significant operational risk.

Spending tells a story. While insurers recognize that they must address operational costs, they continue spending large portions of their budget on legacy with a patchwork of enhancements to try to address today’s market demands, but patchwork legacy solutions struggle to leverage the data held to provide meaningful, actionable insight or ingest new data sources to improve decision-making.

The lack of movement in replacing core with next-gen cloud solutions is now coming home to roost in the growing operational and business challenges. To conquer growing issues like risk volatility, economic resiliency, and talent shortages/ misalignment, insurers need to call on technology. New technologies will help them deal with the core issues, but will also relieve core pressures by improving operations expenses, service levels, and capabilities.

Industry leaders are changing the rules of insurance by leveraging the powerful next-generation intelligent core platforms to launch a new business operating model with new products and then converting business that is part of the future to enable speed and scale.

Insurers must develop a comprehensive strategic response that balances today’s business with what is needed to compete. The underpinnings of the legacy debt and architecture are an unstable foundation for the business to survive, let alone succeed. Can insurers let go of the legacy debt that is holding them back?

Trend 2: Robust Growth in Excess & Surplus Lines and MGAs

Managing general agents in the US market saw very strong growth in 2022, well above the broader property/casualty insurance market growth, according to Conning’s 2023 annual MGA report. With direct premiums written rising 24% as compared to 2021, MGA growth outpaced the overall P&C market by 10.5% with $85.5B in 2022. In addition, the E&S market grew 17.5% in 2022 following 28.8% growth in 2021, highlighting a red-hot market for MGAs and E&S.[ii]

Supporting this growth is the access to capacity and capital from new funding approaches including insurance-linked securities, collateralized reinsurance, reciprocal exchanges, insurers, reinsurers, and private equity. The growth is a recognition of the opportunity for MGAs to help insurers and reinsurers grow their premium, expand into new markets and geographies, leverage underwriting expertise, and leverage a new business model and technology foundation that offers greater speed to market capabilities. This is a key reason why MGAs are attracting top talent, from underwriters to technology professionals, and a reason that some insurers need to seek a new technology foundation.

With the growing volatility of risk, insurers pulling out of markets, and increased insurance exposure across many lines of business, MGAs and E&S products are uniquely positioned to meet these challenging demands. They are innovating and creating new digital business models that provide new products and experiences for customers, particularly for those in volatile risk markets.

With the projected continued volatility and significant market challenges, strong growth in both MGAs and E&S will likely continue to outpace overall P&C growth for the foreseeable future, offering insurers solid alternatives for market expansion and growth. But for traditional insurers and reinsurers to assist MGAs and support growth in E&S areas, it requires more than a desire to expand. It requires an ability to apply expertise and utilize modern product development and data analytics capabilities. Can insurers shift gears to drive growth with MGAs or shifting to E&S products through tech and operational transformation?

Trend 3: Channel Expansion and Ease of Doing Business

While agents and brokers remain a dominant channel, new channels, such as marketplaces and embedded insurance, are gaining a lot of attention and traction. Insurers looking to compete will find it challenging to do it alone. Creating an ecosystem of interconnected channels, using a range of digital capabilities, and connecting with customers when and how they want to, requires collaboration and a willingness to let go of traditional mindsets.

In today’s interconnected world, insurance must play across a wide spectrum of distribution options, expanding channels and partners to reach customers when, where, and from whom they want to buy insurance. These options form a distribution ecosystem that expands the reach but requires a partnership approach, particularly for embedded channels.

In the Majesco-commissioned Celent research report, Reshaping the Distributor Insurer Relationship, it notes that to become the agent’s preferred insurer, the insurer has to have great services, good pricing, and differentiated products, as well as policies, procedures, and technology that make it easy to do business.[iii] Investments in digitization have two potential sources of return. They reduce costs due to the ability to automate processes. They improve an agent’s ability, desire, and ease of doing business with an insurer, therefore driving growth.

The growing spectrum of channel options and opportunities for embedded insurance, as well as the fight for agent/broker loyalty, demand insurers to both expand and optimize their channels to meet growing expectations from both customers and agents/brokers to achieve the growth potential. Can insurers improve the ease of doing business while optimizing channels to attract and retain the best distributors to ensure continued growth as the channel landscape shifts?

The Future Talks

If the future of your business could talk to you, what would it say? Would you be listening? Are you listening?

It’s the right time to figure out what is important — what your company does and does not have to be. Like small businesses enabled through technology, insurers should become more comfortable with the idea of letting go of legacy systems and their burdensome overhead to establish a foundation that builds the business through operational and strategic innovation.

The advantage of next-gen intelligent core systems and other Majesco insurance is that they do so much more with so much less. While keeping your vital operational functions in-house, their accompanying systems, data and security are blissfully relocated on the Majesco cloud platform, where they thrive with improved access, better functionality and they cost less. If improving your ecosystem and its capabilities is important, Majesco’s EcoExchange is a plug-and-play environment with today’s most remarkable insurance tools. Learn how Majesco accelerates operational innovation by placing the best insurance capabilities into your hands.

Are you ready to let go of all that is holding your company back? Are you ready for the future? Contact us today.

By Denise Garth

[i] Manly, Justin, et al., “Most Innovative Companies 2023: Reaching New Heights in Uncertain Times,” Bostom Consulting Group, May 2023, https://media-publications.bcg.com/BCG_Most-Innovative-Companies-2023_Reaching-New-Heights-in-Uncertain-Times_May-2023.pdf

[ii] “U.S. MGA Market Grows Swiftly, Exceeds $85 Billion in Premium in 2022,” Conning, July 24, 2023, https://www.conning.com/about-us/news/ir-pr—2023-mga

[iii] Carnahan, Karlyn, “Reshaping the Distributor Insurer Relationship: A Survey of Independent Insurance Agents,” September 20, 2021, https://www.majesco.com/white-papers/reshaping-the-distributor-insurer-relationship/

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses  NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution

NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution  Leadership Change at Vantage: Former Arch Execs Grandisson, Gansberg to be Chair, CEO

Leadership Change at Vantage: Former Arch Execs Grandisson, Gansberg to be Chair, CEO  Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois

Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois