Property-catastrophe reinsurance rate declines are continuing to taper off from the double-digit average drops that were recorded two years ago, JLT Re reported in a report yesterday.

JLT Re’s Risk-Adjusted Florida Property-Catastrophe ROL Index fell by 3.1 percent this year, compared to 8.5 percent at June 1, 2015 and 17.1 percent in 2014.

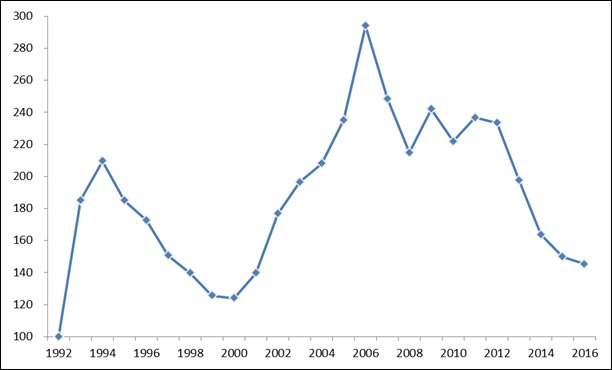

Source: JLT Re

The latest decline in average reinsurance rates marks the fifth consecutive drop in rates at June 1 renewal, but reductions slowed significantly compared to previous years, Bob Betz, co-leader of JLT Re’s National Catastrophe Practice, said in a statement.

“Risk-adjusted pricing typically fell within a range of flat to down 5 percent as markets generally held firm against attempts to negotiate higher discounts. Indeed, efforts to achieve reductions in excess of 5 percent on any one layer were met with considerable resistance,” he said.

Betz also noted evidence that pricing levels between traditional and insurance-linked securities (ILS) markets are converging, “reversing the decoupling trend that first emerged in 2013 when ILS investors deviated away from price expectations set by the traditional market.” While the consensus meant that most programs renewed within a narrow range—flat to low single-digit reductions in 2016—Betz said that “changes to terms and conditions added to the overall economic benefit of cedents in some instances.”

JLT also highlighted three other key midyear developments around pricing, demand and underwriting discipline:

- Pricing for Florida business is approximately 38 percent down on 2012 levels and only 17 percent above the previous cyclical low of 1999/2000, implying limited scope for further profitable pricing reductions.

- There is stable demand for reinsurance cover (after a significant increase last year) as reduced placements by some state-backed insurers was offset by increased appetite within the private market.

- There is evidence of increased underwriting discipline amid margin compression, deteriorating results, increased catastrophe activity in the first five months of the year and predictions of elevated hurricane activity in the North Atlantic due to the potential onset of a La Niña event.

Separately yesterday, Colorado State University affirmed its forecast for an average Atlantic hurricane season as the “current weakening El Niño is likely to transition to weak La Niña conditions by the peak of the Atlantic hurricane season.”

The CSU forecast is predicting 12 in-season named storms (14 including Alex and Bonnie, which formed prior the start of the hurricane season on June 1), 5 hurricanes (six including Alex) and two major ones. “We anticipate a near-average probability for major hurricanes making landfall along the United States coastline and in the Caribbean,” the forecast says.

Still, the trend towards pricing stabilization in the reinsurance market is expected to persist for the remainder of the year, said David Flandro, Global Head of Analytics, JLT Re, noting the pockets of increased reinsurance demand and a series of catastrophe losses already this year.

At the same time, on the supply side, Flandro said, “Surplus reinsurance capacity continues to contain any prospect of higher reinsurance rates.” At the end of the first quarter of 2016, JLT Re estimated dedicated sector capital to be at record levels having risen to $321 billion from $315 billion at year-end 2015.

It’s still a reinsurance buyers’ market right now, Flandro said. “After one of the most costly starts to the year since 2011 with significant catastrophe losses in the United States, Japan and Canada, and with predictions of an active North Atlantic hurricane season, cedents should consider taking advantage of the competitively-priced capacity currently on offer,” he said.

Lessons From 25 Years Leading Accident & Health at Crum & Forster

Lessons From 25 Years Leading Accident & Health at Crum & Forster  Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford  Preparing for an AI Native Future

Preparing for an AI Native Future  RLI Inks 30th Straight Full-Year Underwriting Profit

RLI Inks 30th Straight Full-Year Underwriting Profit