At an industry conference last month, two insurance executives welcomed news of potential flexibility coming from state regulators as they pursue individual paths to digital and data-driven futures, but they said there are other hurdles preventing industrywide innovation.

“I think the obstacles are guts and the people,” said Michael LaRocco, CEO of State Auto Insurance Companies, responding to a question from Leigh Ann Pusey, president of the American Insurance Association, who was moderating a panel at the Property/Casualty Insurance Joint Industry Forum.

“A lot of companies are kind of comfortable, quite frankly. And you’ve got to have the willingness to make those hard calls—and a board’s support to make those hard calls,” he said, referring to the fact that carrier transitions to digital platforms and the adoption of other technological and analytical innovations come with costs. They “will take some level of investment, both time and money that’s significant,” he said.

“You’re seeing a lot of companies try to get around that by doing strategic partnerships, working with various sandboxes or VCs or other organizations, or trying to go through others to go find” new ideas. “It’s not really a bad strategy,” he said.

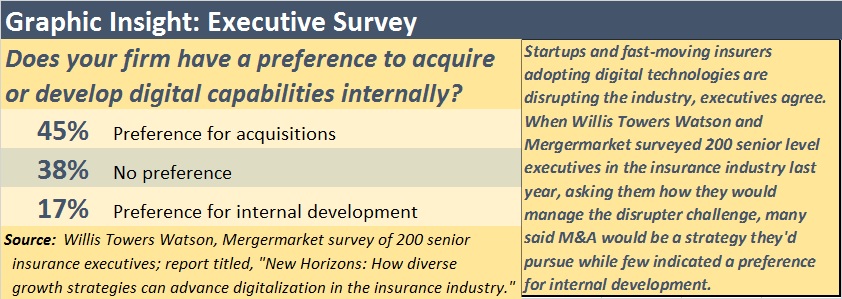

Separately, a few days before the Forum, Willis Towers Watson published results of a survey of insurance executives indicating that less than 20 percent said they had a preference for developing digital capabilities internally.

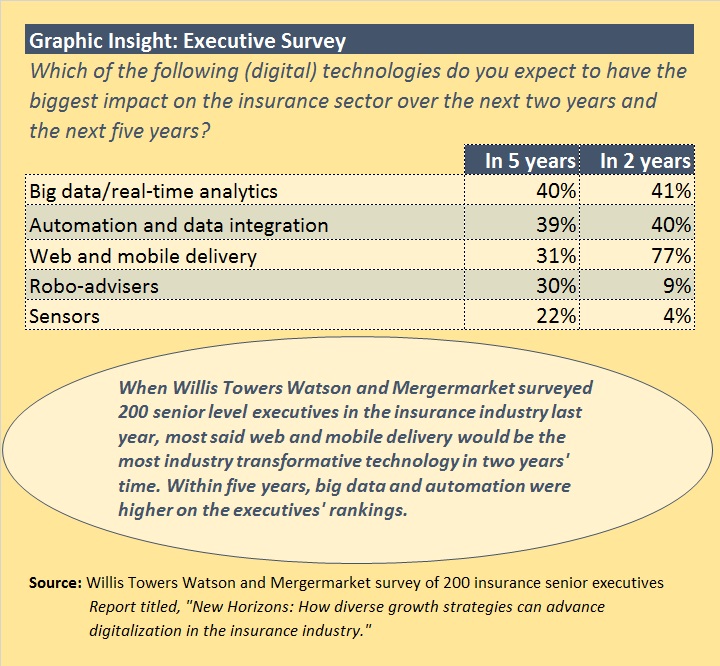

See chart below, which displays survey results relating to other technologies on the horizon, including another potential threat to distribution: robo-advisers.

“It could be bandwidth,” Kuczinski added, picking up on a term that Pusey used to describe a talent shortage as he speculated on another hurdle to insurer innovation. “It could be the demographics of the company. Multiple things.”

Pusey posed her question to the executives following an earlier Forum session during which Ted Nickel, Wisconsin’s commissioner of insurance and the president of the National Association of Insurance Commissioners, vowed to educate his regulatory peers about the cool ways in which insurers are trying to use data and analytics—and convince them to cut insurers some slack. With the breathing room coming from state regulators, and with abundant pools of capital, Pusey wanted to know why insurers aren’t innovating at a faster pace to become more relevant to consumers. “Do we have the bandwidth? The talent?” she asked.

“Our industry faces another coming crisis, which is just a lack of talent,” LaRocco said. “I do think that’s going to be the other potential blocker for us” as an industry, he said.

“As a result, a lot of companies are choosing to do third-party relationships as opposed to trying to build the solutions themselves or find the solutions themselves. There’s risk in that though,” he said, referring to studies that show that 30 percent of U.S. consumers are at least somewhat likely to buy insurance from the likes of Google and Amazon. (See, for example, Capgemini’s World Insurance Report.)

“For folks that say that’s not going to happen, I just don’t agree with that. I believe change is coming. It is inevitable. Companies have to have a strategy to embrace it,” LaRocco said.

Pusey asked hopefully whether moves to embrace technology would attract more talent to the industry.

“It’s going to be a war for talent. We’re not the only industry looking for that talent…This won’t be an easy game.”

“It’s going to be a war for talent. We’re not the only industry looking for that talent…This won’t be an easy game.”

Anthony Kuczinski, Munich Re U.S.

Photo by Don Pollard

Think about “the flip side of that,” he said. “What kind of talent do we have to deal with this new world that we’re dealing with?” If the retiree counts are close to accurate, “they’re probably people not adapting to the new technology.”

Kuczinski did say that the industry is getting better at attracting talent, as more schools focus on risk management and as industry forays into the InsurTech space make it more possible to draw in a new generation. “But it’s going to be a war for talent. We’re not the only industry looking for that talent,” he said. “This won’t be an easy game.”

“I think it’s real. I think it’s something we should be constantly trying to address. There are lots of ways to address that through your benefit programs, and how you pay people, how you expect them to work.”

“The InsurTech changes are real” as well, LaRocco said. “We’ve allowed ourselves [to] be defined by others. Shame on us for that. This is a powerful, exciting, cool industry. We’re not taking advantage of preaching that. We’ve let others define us to some degree.”

“The reality of our crappy technology and our old legacy systems and the old way we do business is part of that problem,” he continued. “It’s not going to be attractive for someone to come to a company and work on a green screen. That’s not going to do it for them.”

A Turning Point Opportunity

“This is a turning point opportunity,” he told fellow executives in the audience, noting that while his company has done the “easy stuff,” like eliminating dress codes and annual performance reviews, there might be a bolder step to take. “People may laugh, but maybe you do start defining yourself as a technology company whose product is insurance, or as an InsurTech company whose critical importance is protecting lives, homes and autos in a hi-tech manner.”

If existing insurers don’t start defining themselves in that way, other companies will leap to define themselves in that fashion instead. “You’re seeing that now. [InsurTech startups] are presenting themselves differently and trying to break through some of the old and unfortunate definitions that people have put on us.”

“Maybe you do start defining yourself as a technology company whose product is insurance, or as an InsurTech company whose critical importance is protecting lives, homes and autos in a hi-tech manner.”

“Maybe you do start defining yourself as a technology company whose product is insurance, or as an InsurTech company whose critical importance is protecting lives, homes and autos in a hi-tech manner.”

Michael LaRocco, CEO, State Auto

Photo by Don Pollard

One obvious example is the upstart peer-to-peer insurer Lemonade, which has used terms like annoying, antagonistic and dishonest to describe insurers. A member of the Forum audience asked LaRocco to share his thoughts on the technology disrupter, which in the days before and after the Forum had been releasing news about policy counts and claims handling, marketing the news releases as “Transparency Chronicles.”

“The shared economy is real. And the possibility of this next generation of insurance buyers wanting to get their insurance products…in a very different way is real—whether they’re insuring moments in time, or [there is] the ability to insure somebody when they’re driving at a certain point on a road,” he said, referring to the on-demand insurance aspect of some InsurTechs, in addition to Lemonade’s peer-to-peer sharing.

Referring to Lemonade specifically, he said: “I think the public relations around it and marketing have been the best part of it. I congratulate them on that. Quite frankly, I don’t really understand it even though I’ve read about it. So, I can’t sit here and suggest that I think it’s going to be a winner or a loser.

“Good marketing and good P/R will work for a while. Whether that will sustain itself, we’ll have to find out. But I don’t dismiss the idea of some type of shared economy solution to insurance. That is the way people need to be thinking in this room…We have to be thinking about the possibilities that are far outside and prepare for those things. That’s the challenge that we face.”

Kuczinski said he had nothing further to add other than “what’s the harm in continuing to explore, to be part of these things, quite frankly to create our own intelligence base. To ignore it would be wrong too. Our view has been let’s embrace these things. Let’s learn from them. If in fact they take off, we’re that much further along. If not, it’s R&D.”

Embracing Change and Changing Speeds

- Next Insurance, Munich Re to Offer Coverage for Commercial Photographers (December 2016)

- Munich Re Partners with InsurTech Startup Wrisk (November 2016)

- Trov Teams With Munich Re for 2017 U.S. Launch of On-Demand Insurance Platform (September 2016)

- InsTech Startup Slice Partnering with Munich Re (July 2016)

- Munich Re Links with Drone Company to Quicken Catastrophe Insurance Assessments (May 2016)

Munich Re is a reinsurance provider for Lemonade, and Munich Re and Munich Re, US are among the most active investors and partners in the InsurTech space. Besides making investments through Munich Re/ HSB Ventures and Digital Partners (a Munich Re program founded in May 2016 to offer international insurance capacity, insurance product development expertise, technology and venture capital funding to emerging tech startups selling insurance), in the United States, Munich Re, US has set up an internal innovation lab and two risk incubators to study autonomous vehicles (and mobility generally) and insurance on-demand.

“We are totally embracing it,” Kuczinski said, noting that the speed of technological change demands that insurers be proactive. “There isn’t going to be the time [to react]. What used to take 10-15 years is not going to be that long anymore,” he said, explaining that big data, digitalization and the Internet of Things are all combining to create much faster turnaround times than insurers are used to dealing with.

“As an industry, we have always innovated. There’s not a product we offer today that at some point in its evolution wasn’t a new product that we learned how to adapt to the current environment. The single biggest difference today is the speed,” he said.

Separately, Kuczinski urged insurers and reinsurers to drive their own disruption and participate in the digital transformation of the economy in an article he wrote for Carrier Management last year, “CEO Viewpoint: Challenge of Disruption Awakens a Sleeping Giant,” also describing his company’s efforts to get closer to disrupters in innovation hubs like Silicon Valley, Tel Aviv and Berlin.

“I do think that regulatory issues will be some of the slower parts of this,” he added. “But I think it’s incumbent upon us…to educate our regulators.” But regulators aren’t the only parties that need advice, he maintains. “What we try to communicate to the newcomers, the InsurTech firms, is if you just offer the same product faster but for the same cost and there’s nothing taken out of the equation, then it’s game over. It’s not going to happen. Why would a regulator respond to that?”

A regulator might respond if there’s five points taken out of the equation, or seven points,” with expense cuts from efficiencies translating into lower insurance costs to consumers, he said.

Referring to comments made by participants at an earlier Forum panel, LaRocco said that the idea that driverless cars will be on the road in five to 10 years is “insanity. It’s going to be much, much sooner than that,” he believes.

“I think we’re on the cusp of truly dramatic change,” he said, going on to dismiss the popular idea that changes of a digital, data-driven world are only going to disrupt the personal lines side of the business. “The business that’s ripe for a complete transformation is commercial lines. It’s old. It’s not innovative and there are data aggregators out there now that are creating information around businesses that we can leverage,” he said.

Moving past the segment-specific analysis, Pusey noted that an “astronomical” amount of money is being spent on InsurTech by “really smart people that are looking at our industry and saying this is a good opportunity to do something different and transform it.”

“And part of what they look at is the average cost to the industry,” said Kuczinski, finishing her thought and noting that the expense component of the premium dollar is 35-40 points. “Can I do that better?” they ask. And they don’t have to spend the whole 35-40 points. They want to find a way to do it much quicker, much easier. They get it.

“And then how do I empower that customer who wants what they want, when they want it, where they want it for only when they want it?” Technology is allowing this all to happen,” he said.

LaRocco said State Auto has made its own moves to prepare for the “completely digital world” that is on the horizon. “We’ve launched our first five states for home and auto completely digital. There’s no paper. There’s no checks. There’s no cash. If you want to buy a policy, you either give us your credit card or your checking account. And everything is e-signature.

“It’s a risky move in some ways, but the reality is if you look at the way things are changing, the way things have evolved, Macy’s, Sears and Kmart are basically dead, and Amazon is doing more business than them,” he said. The power of the change that’s coming to our industry is much, much bigger than we’re seen before. We’re embracing it and try as best we can as a little company out of Columbus, Ohio.”

Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday

Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday  Beazley Agrees to Zurich’s Sweetened £8 Billion Takeover Bid

Beazley Agrees to Zurich’s Sweetened £8 Billion Takeover Bid  RLI Inks 30th Straight Full-Year Underwriting Profit

RLI Inks 30th Straight Full-Year Underwriting Profit  Modern Underwriting Technology: Decisive Steps to Successful Implementation

Modern Underwriting Technology: Decisive Steps to Successful Implementation