A.M. Best is overhauling the calculation of the Best’s Capital Adequacy Ratio used in its assessments of insurer capital strength, but higher resulting risk charges and correspondingly lower BCAR scores for property/casualty insurers, will not mean widespread rating actions.

[ijtv id=”13234″ width=”340″ float=”right”]In fact, because stochastic modeling of risk factors creates a better, “more robust” tool, analysts will be thinking about the BCAR results differently, according to A.M. Best Executive Vice President and Chief Operating Officer Matthew Mosher. In advance of the planned March release of the BCAR calculation draft, Mosher sat down with Carrier Management, explaining that while the BCAR update was essentially complete last autumn, the release process has been slowed down as analysts reworked the Best Credit Rating Methodology too—helping insurers to understand how the new BCAR will fit into the rating process.

“As a starting point, the industry is very well capitalized. So capital is not really a ratings driver. When you look at our overall methodology, our view is that our ratings are appropriate right now,” he said.

“We’re strong believers in the fact that the model are tools, and they’re going to provide you with information. But you have to use the most important one, that’s your brain, to understand and make a judgment for what your view of capitalization is for a company,” he added.

Mosher said that once the BCAR draft is out (expected to happen in early March), the comment period is will last several months for the property/casualty BCAR and also for the life/health BCAR and the universal BCAR, (used to composite‑type companies outside of the United States). “All of those comment periods tie in. They all have to be wrapped up along with the methodology comment period. Our target for that is the beginning of 2017.

“So there’s a pretty lengthy comment period. You don’t need to be reacting ahead based on rumor or what you think is coming. Wait until you see what’s out there.”

Q: Why did A.M. Best decide to update the BCAR model?

Mosher: First and foremost is the amount of data. The technology advancements since we had made any major updates to the model have changed dramatically. We had the ability to get better insight and a better understanding of a company’s risks by making this update. Given the better data, better technology, and getting better information, we felt it was the time to do it.

Q: Beyond the fact that the new BCAR model is a stochastic model rather than a factor-based model, what are some of the other key changes to the BCAR calculation?

[ijtv id=”13232″ width=”340″ float=”right”]Mosher: One of the biggest enhancements that we have is now that the risk factors across the different risk elements—whether for assets, underwriting risk, or credit risk—are all more consistently tied to a value-at-risk measure.….

The other major improvement is that we’re looking at it at multiple confidence levels. Historically, the model was loosely tied to a 99 percent confidence interval. Now, we’re looking at a 95 percent confidence interval, a 99 percent confidence interval, 99.5 percent, 99.8, and 99.9.

We have five different confidence levels and we go much further out the tail. When you look at a 99.9 percent confidence interval, you’re at 1-in-1,000-year type of loss as opposed to 1-in-100 year. So, it shows the level of protection a company has to the tail events that they’re exposed to.

We’ve always captured that, at least for property-catastrophe type of exposures. We’ve always captured it in our SRQ [supplemental rating questionnaire]. But this brings it into the calculation, and it’s much more clearly seen…

Another big issue is we’ve brought the probable maximum loss [for] the catastrophe exposure in—we now treat it as a risk. It is in the net required capital as opposed to being an adjustment to surplus. And we kept it outside the covariance so that it still doesn’t get correlated away. The reason for that is just because it’s such a major risk for companies. Catastrophe risk is a major risk that we’ve seen have an impact over the years on companies.

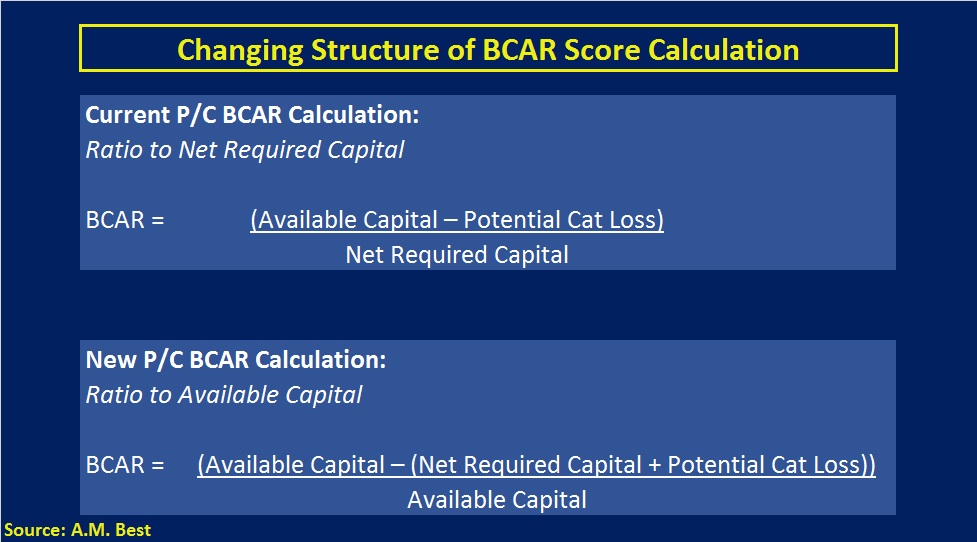

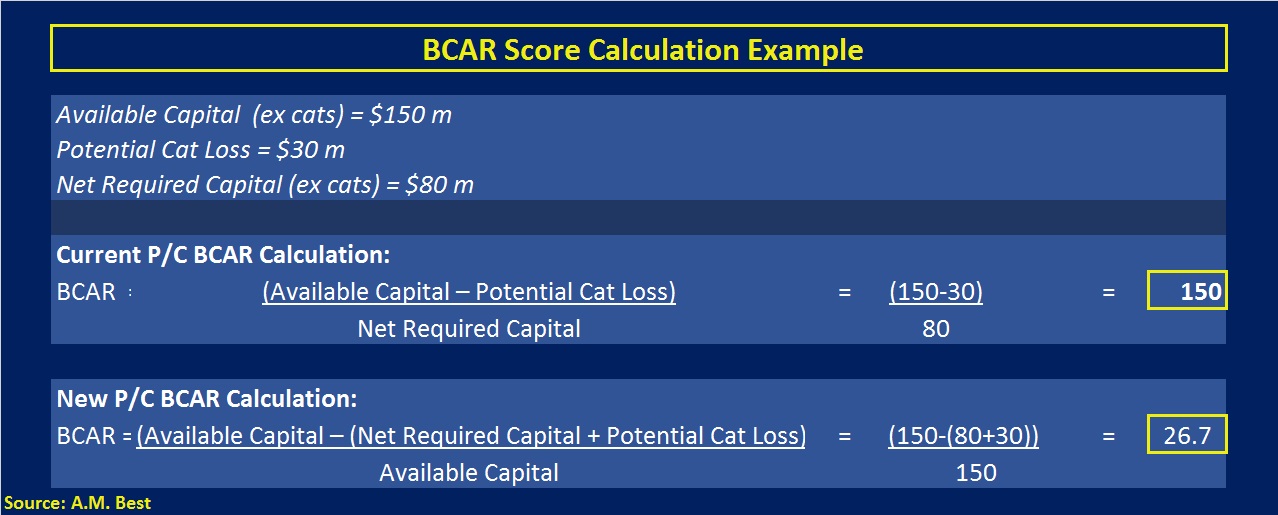

Then finally we did change the score calculation. It used to just be available capital divided by net required capital, which would say that if you had available capital to adequately meet your net required capital, you got a score of 100, i.e., you had 100 percent of net required capital.

Q: Why change the structure of the calculation?

Mosher: We’ve adjusted that for a couple of reasons. One, they are two different models. We didn’t want people trying to compare scores or [asking], “What happened to my score?”

…Now, it’s done as a percentage of available capital. The calculation now is available capital minus net required capital divided by available capital. So, if your available capital is 10 percent larger than your net required capital, you’re going to end up with a score of 10. If it’s equal to, you’re going to end up with a score of zero. A zero is the old 100. If you have less capital than is required based on net required capital, you’re going to have a negative score. It allows a better idea comparing to what percentage of the capital you’re holding as opposed to calculated net required capital.

Another piece, too, is we feel this is a much more robust model…. You won’t see the kind of cushion that’s in there above the required scores that are in there now.

If you look at the median scores, the median scores are over 200, yet the [current] guidelines say 175 [equates to implied balance sheet strength of A++]. A lot of that reflects a company’s operating performance, its business profile, and risk management. What we’re doing is reworking our rating methodology that [describes] how BCAR fits into the overall methodology.

Q: So A.M. Best will no long publish guidelines that say if you have score X, you get A+ or score Y, gets you A++.

Mosher: That’s because capital never could get you to A++. You also had to have good operating performance, good business profiles.

Now, what we’re saying is capital brings you only so high up the scale, and to get to the highest levels you have to have operating performance that increases our view of the company. And you have to have a business profile that increases the view of the company, and risk management, and so forth. It’s a little bit different view in looking at the application of BCAR.

Obviously companies are concerned about their rating. That’s the important piece. We wanted to wait and make sure we put out the updated methodology in terms of how the BCAR was going to be applied in the rating methodology and in the rating process. That’s why we slowed it down.

Probably the biggest feature when we update our new methodology and how that [BCAR] model fits in the overall methodology, is the view that this is a model. It’s a tool that we have as the analysts. We’re not looking at what’s a passing score for this model to get you to a given rating. It’s a tool that evaluates a piece of your overall rating. That’s probably the most important part of the overall change that we’re making.

Q: The new tool actually produces five BCAR scores at different confidence levels. How will analysts interpret five scores? Will some companies (reinsurers and large global insurers, perhaps) be assessed at higher confidence levels?

Mosher: No, we’ll be looking at all five….The scores are viewed the same for every type of company.

The old model was probably equivalent to a 99 percent confidence interval. Now we look at a range of scores at the 95, 99, all the way up to 99.9.

We’re not necessarily looking at how high does the score go at one of those confidence intervals. What we’re going to be looking at is how high of a confidence interval do you have a passing score at. That will give us an idea of, based purely on your statutory capitalization, how strong you are.

When we view the overall balance sheet strength, we’re going to look at the trend line in terms of how quickly do you fall off [or does your score turn negative]. Usually that’s a property-catastrophe type of issue. Your reinsurance ran out.

The quality of the capital, the dependence on reinsurance is going to be an important piece as well….

The important thing is, we can’t just pick one of those scores and publish it because looking at one of those scores tells you one thing: Where are they in the confidence interval for that score. It doesn’t tell you about the next one where risk might dramatically increase. So we have to look at the trend across the scores [to] get a feel for how well [an insurer] deals with its tail risk.

Q: During the BCAR webinar updates from A.M. Best, there was some discussion about the rating process including an assessment of dependence on reinsurance. Is that new?

Mosher: The calculated piece for dependence on reinsurance was always there. It reflected your recoverables from reinsurers. If the recoverables were too high, you got an additional charge, which was for a dispute risk. You have the credit risk but also the reinsurer might say, “No, I disagree. I’m not paying.” If you look at Legion way back, that was one of the major issues. Their ceded leverage was [near] 20-times surplus. When they had 2 percent of their recoverables disputed, that wass 40 percent of the surplus disappearing…..

That’s always been [considered] in the [our calculation]. The second piece to it is this idea of the property-catastrophes. How high is your gross PML [probable maximum loss] versus your net PML? Let’s face it. If you have a huge gross PML, and you only brought to 1-in-100 years, you might fail the 99 percent confidence level right after. You can turn around and buy more reinsurance. But, that makes you dependent on being able to get that reinsurance year after year…You’re dependent on the fact you can renew your catastrophe treaty every year.

This [approach] really takes the view that reinsurance is a form of capital and it’s a fairly short-term form of capital. It’s a one-year term form of capital basically. So, if you’re heavily dependent on reinsurance taking away a significant part of your risk, particularly property-catastrophe risk, that’s going to be a qualitative factor in our assessment of your overall capitalization. Even though your score will pass all the way at the 99.9, if you’re so dependent on that reinsurance, we’re going to then discount that in our evaluation of the company.

Q: Based on your interactions so far, what are insurers and reinsurers most worried about or most confused about? Have you made any changes based on what feedback you’ve heard?

Mosher: We slowed down the [BCAR] release, making sure we put out how it was being applied along with the calculation.

There are some concerns that there will be additional capital requirements because scores [are worse]. That’s one of the reasons that we’ve told people over the last few months to wait until they see how the [BCAR] model is used in the overall rating methodology.

We recognize the fact that there are some scores that may change. But those BCAR scores mean something different. Our view of the model is that it’s much more robust. Your BCAR score might go down, but it doesn’t impact what that BCAR score means to the overall rating because our view of what’s necessary for a rating has changed as well.

In part 2 of the interview, Mosher talks more about the stochastically modeled risk factors, which ones are moving the most in the calculation, and how A.M. Best analysts will consider results from insurers’ internal capital models. See related article, “Understanding A.M. Best’s New Capital Model: Matthew Mosher Q&A (Part 2).”

Other related articles:

Related Videos: