The story of U.S. personal lines challenges impacting the results of multiline insurers was repeated for Liberty Mutual, which reported underwriting losses and waning policy growth in the segment in 2022.

President and Chief Executive Officer Tim Sweeney reported overall drops in net income for Liberty Mutual Holding Company’s fourth-quarter and full-year 2022 on Thursday, principally related to changes in investment returns, as well as overall jumps in companywide premiums driven by two acquisitions: State Auto in the U.S. and AmGeneral in Malaysia. He also highlighted developments in U.S. personal lines.

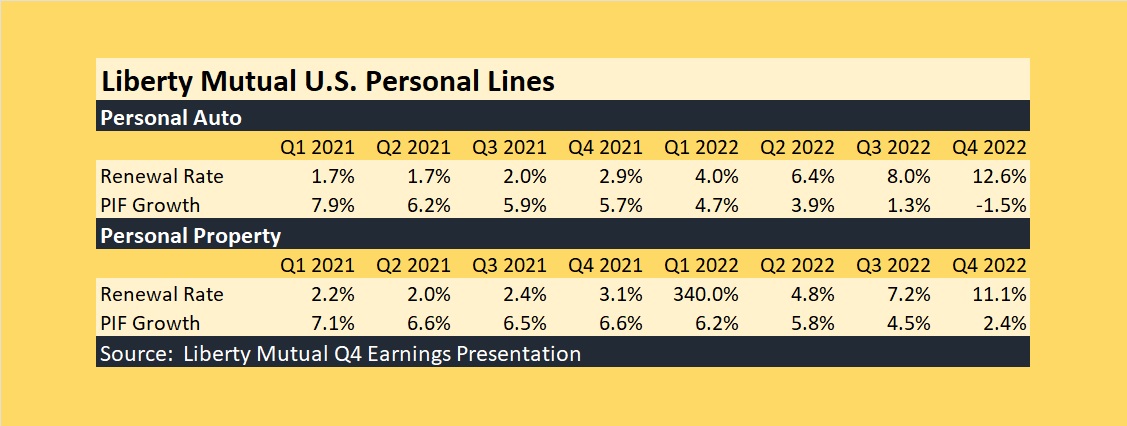

“Our focus in U.S. personal lines is on rate adequacy, and so true exposure growth continues to be limited, evidenced by a 1 percent reduction in private passenger auto policies in-force [in the fourth quarter] and slower growth in property PIF [policies in-force],” Sweeney said, leading his first earning conference call at the helm.

Sweeney and James M. MacPhee, president of Global Retail Markets, reviewed renewal rate changes for personal auto—rising from 2.9 percent in fourth-quarter 2021 to 12.6 percent in fourth-quarter 2022, with retention falling only slightly from 79 percent to 77 percent. At the same time, PIF growth reversed from 5.7 percent in fourth-quarter 2021 down to 1.3 percent in third-quarter 2022, and to negative 1.5 percent in the final quarter. Similar rate changes in homeowners brought PIF growth down from 6.6 percent for fourth-quarter 2021 to 2.4 percent in fourth-quarter 2022.

“The bigger impact is to new business, which is down about almost 20 percent year over year by the end of the fourth quarter,” said MacPhee, explaining the drop in policy counts vs. the stable retention figures.

“2022 proved to be a very challenging year for U.S. personal lines insurers in particular, driven by inflation affecting loss costs that remained elevated over historical levels through the fourth quarter. We have taken significant action to overcome these adverse trends, including substantial rate and tighter underwriting and media spend reductions to strategically slow policy growth, particularly in the most profit-challenged markets,” MacPhee said in his opening remarks. “The impact of these actions has grown throughout 2022, and we have momentum to build on here for 2023.”

Still, net written premium for retail markets, which also includes U.S. small business and personal lines globally, jumped 16 percent in the quarter and for the full year. MacPhee noted that excluding the impact of the acquisitions and foreign exchange, the premium increase would have come in at 7 percent.

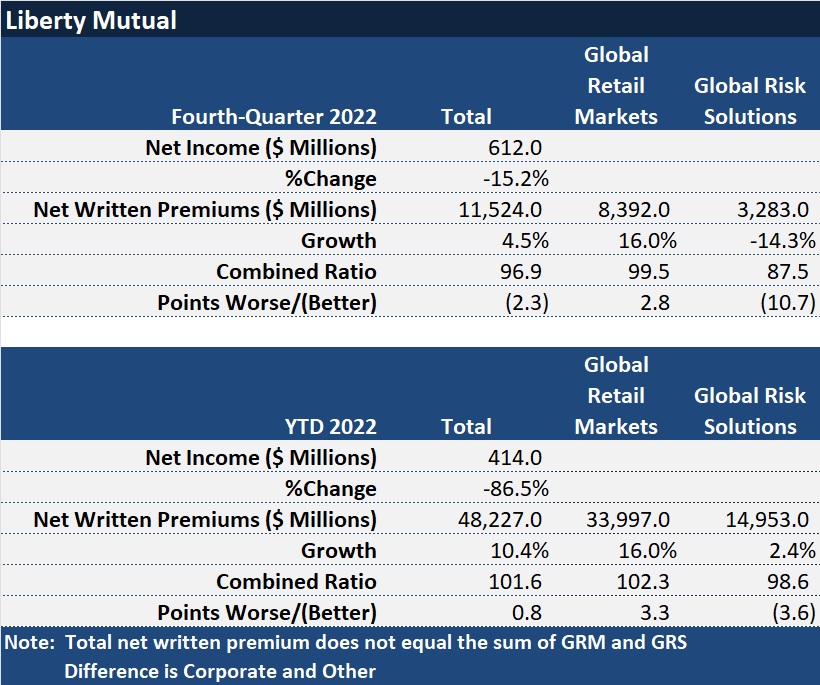

For Liberty’s commercial, specialty and reinsurance businesses—referred to as Global Risk Solutions—premiums shrank 14.3 percent in the fourth quarter and grew just 2.4 percent for the year. Sweeney and GRS President Neeti Bhalla Johnson attributed part of the drop to reinsurance program changes. While Bhalla Johnson described individual segments with premium growth, including a 9.7 percent jump in GRS North America (mainly attributable to a loss portfolio transfer with an existing customer) and others with intentional derisking (like Liberty Mutual’s assumed reinsurance business where premiums dropped 14.7 percent), overall, she commented that renewal premium rate increases exceeded loss trend in 2022 (6.6 percent vs. 5.5 percent). “We expect aggregate rate increases to exceed the aggregate loss trend in 2023, though not as positive or as uniform as in recent years,” she said.

Global Risk Solutions recorded underwriting profits for both the fourth quarter and the year. Bhalla Johnson said that a 10.7-point improvement to 87.5 in the final quarter was driven by favorable catastrophe loss development on events occurring earlier in the year and prior accident year weakening in Q42022 versus strengthening in Q4 2021.

While the Global Risk Solutions full-year combined ratio improved 3.6 points to 98.6, the combined ratio of Global Retail Markets deteriorated by a similar amount—3.3 points to 102.3. Excluding the impact of catastrophe losses, the loss ratio rose by 5.0 points, but an improved expense ratio (0.9 points) and favorable prior year development helped to dampen the impact of the loss ratio deterioration.

For the holding company overall, bottom-line net income fell to $414 million, down from a record figure of $3.1 billion in 2021. Sweeney and Chief Financial Officer Christopher Peirce explained that the decline was driven mainly by significantly lower returns from limited partnership investments.

Ignoring that impact, pretax operating income before limited partnerships income for the year was $593 million, down 10.7 percent from $664 million in 2021. Peirce said this was primarily driven by higher catastrophe losses including losses from State Auto and was partially offset by lower severity and prior-year reserve releases in Global Retail Markets. The decline is 7.7 percent excluding the cat and prior-year development impacts, he said.

[inline-ad-1]