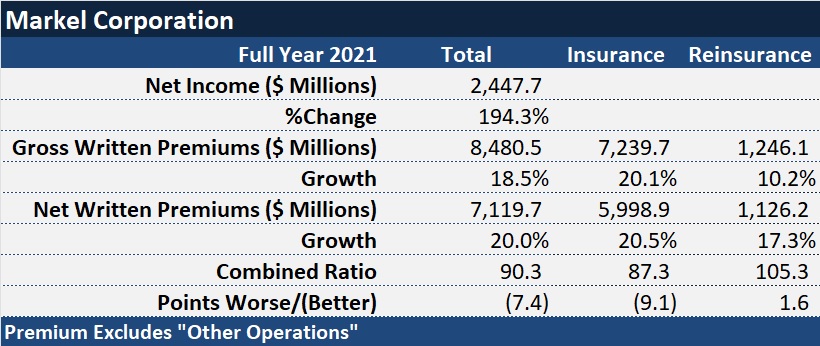

Markel Corporation reported a “record-smashing” $628 million in underwriting profit for 2021, a figure that translated into a combined ratio of just over 90 for the year.

Co-Chief Executive Officer Richie Whitt said the 90.3 combined ratio was the fourth lowest reported by the company in 30 years during an earnings conference call Thursday.

On the top line, gross premiums grew 18.5 percent to $8.5 billion, putting the company on track to achieve a “10-5-1” target put in place last year—a goal to reach $10 billion in premium within five years with an annual underwriting profit of $1 billion, he said.

Actions to remix the Markel portfolio and reduce exposure to natural catastrophes were part of the formula that helped specialty insurance and reinsurance operations record a 7.4-point decrease in the overall combined ratio compared to 2020. Catastrophes had the same impact on Markel’s 2021 and 2020 combined ratios, adding 3 points to both, according to Chief Financial Officer Jeremy Noble—even though industrywide catastrophe losses surpassed $100 billion in 2021.

“In 2021, our strategy to manage the impact of nat cat volatility worked,” said Whitt, noting that the 3 points was a significant decrease from the average annual impact experienced in prior years.

In late 2020 and early 2021, Markel executives previously reported that the company was significantly reducing writing insurance and reinsurance with exposures to natural catastrophes. One decisive action came in late 2020, when the company announced it would discontinue writing catastrophe-exposed property in its reinsurance segment on a risk-bearing basis, instead allowing its Nephila insurance-linked securities operation to start placing the business with third-party capital providers, effective Jan. 1, 2021.

Noble reported that, besides 3 points for catastrophe losses, the prior year’s combined ratio also included 6 points related to COVID losses. Excluding the loss impacts of catastrophes and COVID-19 in both years, Markel’s consolidated combined ratio dropped to 87 in 2021 compared to 88 for 2020, he said, noting that a favorable pricing environment and the impact of underwriting actions taken to enhance our profitability pushed the non-cat attritional loss ratio down 4 points, while a lower level of favorable prior-year development pushed the ratio in the other direction.

Even with reductions in property-exposed business, Markel saw premiums grow by double-digits in both the insurance and reinsurance segments.

Gross written premiums from reinsurance operations grew by 10 percent in 2021, with the emphasis now on casualty and specialty business.

Primary insurance gross premiums jumped 20 percent, with new business opportunities in professional liability and general liability, together with favorable rate environments across most insurance product lines driving the increase, Whitt said.

But Markel executives aren’t banking on favorable market conditions to continue indefinitely.

“Let’s be honest, we don’t know what the market will look like in future years, and it may not be as strong,” said Whitt at one point. Reporting that the company is mathematically slightly ahead of the 10-5-1 goal just one year into the plan, “that is a good thing,” he said, referring to the very favorable market conditions of 2021 and early 2022.

“There is no doubt that after three years, and in some cases four years, of rate increases, it’s going to be difficult to continue to average double-digit growth in rates across our portfolio like we did in 2021.”

Richie Whitt, Markel

“We expect to achieve rate increases in the great majority of our lines as we go through 2022,” he said later. But “there is no doubt that after three years, and in some cases four years, of rate increases, it’s going to be difficult to continue to average double-digit growth in rates across our portfolio like we did in 2021,” he added.

“There’s some fatigue creeping in [for] the insureds,” especially in lines that have had big increases, he told an analyst who asked him about renewal retentions later in the call. “As you go through the market cycle, it would not be surprising to see renewal retention start to drop a bit in some of those areas,” he said, highlighting D&O and financial institution lines, in particular.

Firing on All Cylinders Despite ‘Unrelenting’ Conditions

“This call is as fun as it gets,” said Co-CEO Tom Gayner, who started the conference noting that results of insurance and reinsurance underwriting activities weren’t the only reason that net income nearly tripled to $2.4 billion. “All three engines of Markel provided full thrust during 2021,” Gayner said, referring to positive results for Markel’s investment operations and Markel Ventures (a unit that invests in businesses outside of the insurance industry).

“We designed the three-engine approach in order to be able to make progress through thick and thin. That said, it’s more fun to look at the numbers when they are thick,” he said, noting that all three engines were firing in 2021.

“We designed the three-engine approach in order to be able to make progress through thick and thin. That said, it’s more fun to look at the numbers when they are thick,” he said, noting that all three engines were firing in 2021.

Net investment gains included in net income more than tripled to $1.9 billion in 2021 compared to $618 million in 2020. In both periods, net investment gains were primarily attributable to an increase in the fair value of Markel’s equity portfolio, driven by favorable market value movements, executives said.

Gayner noted that Markel Ventures had record revenues of $3.6 billion, up 30 percent from $2.8 billion in 2021, with EBITDA (earnings before interest, taxes, depreciation and amortization) reaching $403 million compared to $367 million, a 10 percent jump.

As he described the growth of the Markel Ventures portfolio, Gayner took time to reflect on the U.S. business environment generally and the accomplishments of the managers of the Venture businesses in spite of supply chain and labor issues.

First, Gayner highlighted two recent additions to the Markel Ventures family: Buckner, an operator of crane rental fleets serving large commercial contractors in the construction of wind turbines, stadiums, manufacturing facilities and other complex projects; and Metromont, a precast concrete manufacturer serving general contractors in the construction of data centers, warehouses, multi-family residential structures, parking decks, and a variety of other commercial structures.

Then he described the experiences of the companies in the Markel Ventures portfolio generally, reporting: “Everything you hear about supply chain problems is real.”

“People and material are…tough to come by, and some of the margin pressures we experienced during the year reflect that reality,” he said.

“A year ago, you heard the word unprecedented over and over. Now…we’re looking at precedented conditions. 2021 results largely compare with 2020 results that took place under the conditions of the pandemic. [But] unprecedented is now morphing into unrelenting,” he said.

“The daily grind of trying to figure out how to keep our team on the field and recruit new players, procure supplies, maintain margins…is unrelenting”

Tom Gayner, Markel

In addition to Gayner’s reports of results for Markel Ventures and investment activities, Whitt reported results of insurance-related activities that aren’t included in the premium and combined ratios figures summarized above: the ILS operations and program services operations.

Program and fronting services, provided through State National, produced over $2.7 billion of gross written premium, a 31 percent jump over 2020, and generated roughly $126 million in fee revenues for Markel, up 21 percent from the prior year. “Despite increasing competition in this segment, we continue to see a strong pipeline of opportunities in the current market,” Whitt reported.